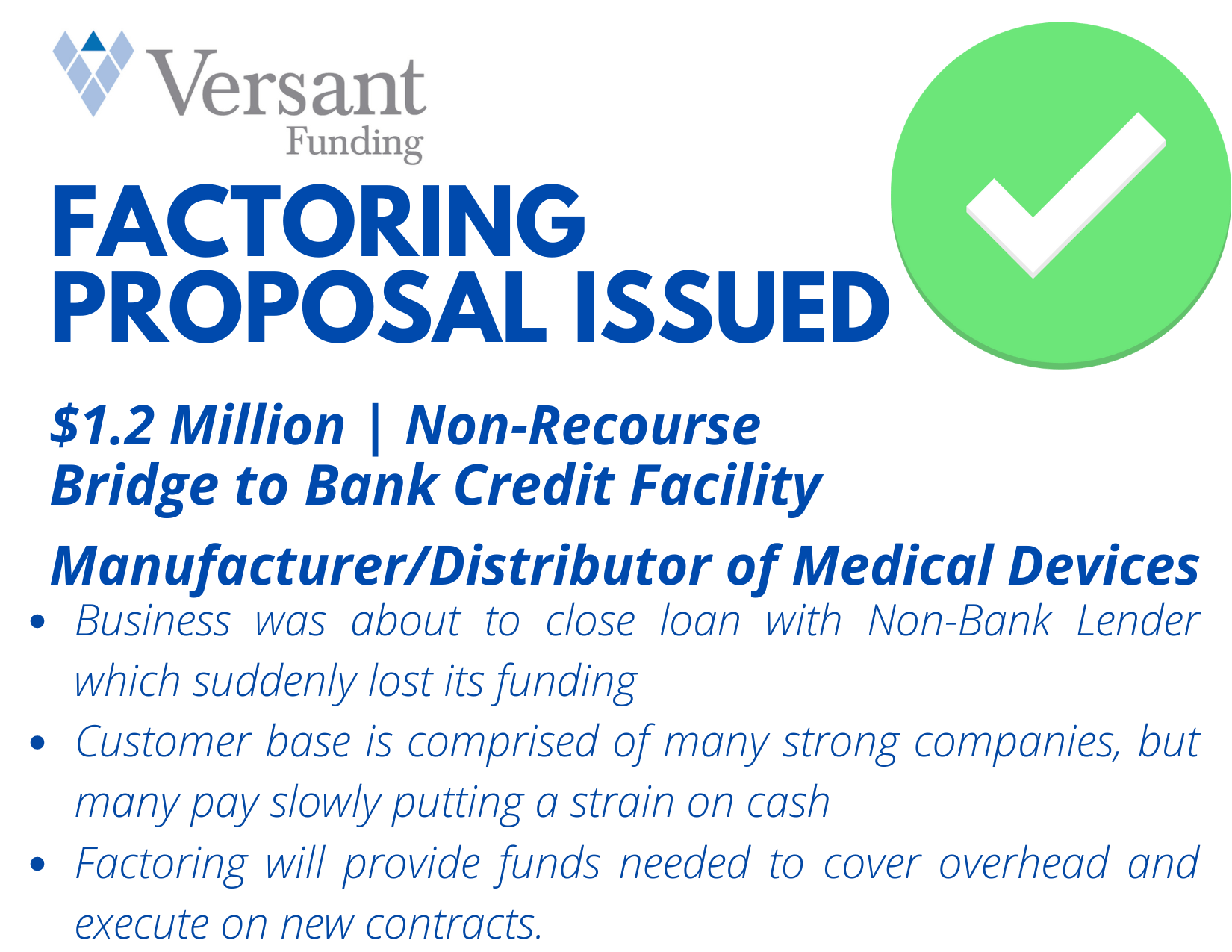

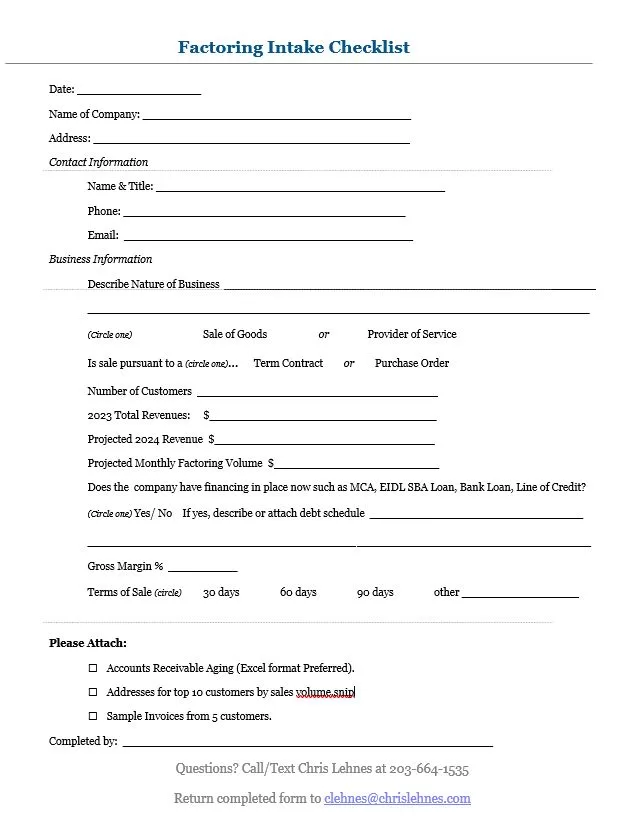

Factoring offering can quickly fund Service Providers(as well as Manufacturers and Distributors)which do not meet traditional lending standards but have good quality accounts receivable outstanding.

The influence of geopolitics on supply chain decisions cannot be overstated. From trade disputes and economic sanctions to geopolitical tensions and pandemics, a myriad of factors constantly reshape the global landscape, presenting both opportunities and challenges for businesses. Understanding these dynamics and their implications is crucial for effective supply chain management.

Geopolitical tensions can disrupt supply chains in multiple ways. Trade barriers, tariffs, and sanctions can restrict the flow of goods and services between countries, leading to increased costs and logistical complexities for businesses. For example, the escalating trade conflict between the United States and China in recent years has prompted many companies to reassess their sourcing strategies and diversify their supplier base to mitigate risks.

Moreover, geopolitical instability in certain regions can threaten the security of supply chains, particularly for industries reliant on critical resources or situated in politically volatile areas. Civil unrest, armed conflicts, or natural disasters can disrupt transportation networks, disrupt production facilities, or cause delays in shipments, impacting the flow of goods and causing disruptions.

The COVID-19 pandemic has further highlighted the vulnerabilities inherent in global supply chains. Travel restrictions, border closures, and lockdown measures have disrupted the movement of goods and labor, leading to shortages of essential products and raw materials. Companies have had to adapt rapidly, reconfigure their supply chains, and prioritize resilience and flexibility to mitigate the impact of future disruptions.

In response to these challenges, businesses are adopting various strategies to navigate the complex geopolitical landscape. One approach is to diversify sourcing and production locations to reduce dependency on a single region or country. By spreading their operations across multiple locations, companies can minimize the risk of supply chain disruptions caused by geopolitical events or natural disasters.

Furthermore, enhancing transparency and visibility across the supply chain is essential for identifying potential risks and developing contingency plans. Leveraging data analytics, digital technologies, and supply chain management platforms can provide real-time insights into market trends, supplier performance, and geopolitical developments, enabling companies to make informed decisions and respond quickly to changing conditions.

Collaboration and partnerships are also crucial for managing geopolitical risks effectively. Building strong relationships with suppliers, logistics providers, and government agencies can help companies navigate regulatory challenges, secure alternative supply sources, and access critical resources during times of crisis.

Ultimately, businesses must adopt a holistic approach to management that integrates geopolitical analysis, risk assessment, and contingency planning into their decision-making processes. By proactively addressing geopolitical challenges and building agile and resilient supply chains, companies can enhance their competitiveness and adaptability in an increasingly uncertain world.

Star Wars Day, observed annually on May 4th, is a beloved occasion celebrated by fans of the iconic Star Wars franchise. This article explores the origins of Star Wars Day and the various ways in which it is celebrated around the world. What is Star Wars Day?

Star Wars Day

Origins of Star Wars Day

The origins of Star Wars Day can be traced back to a pun on one of the franchise’s most famous catchphrases: “May the Force be with you.” The phrase, frequently uttered by characters throughout the Star Wars films, has become emblematic of the series’ themes of hope, bravery, and the mystical Force that binds the galaxy together.

The pun, “May the Fourth be with you,” first emerged as a playful nod to the original catchphrase. It gained traction among fans in the late 20th century, particularly with the rise of internet culture and social media platforms where fans could connect and share their enthusiasm for the franchise.

Evolution of the Celebration

What started as a playful pun among fans quickly evolved into an annual celebration known as Star Wars Day. The first organized Star Wars Day event is believed to have taken place in Toronto, Canada, in 2011, where fans gathered for movie screenings, cosplay contests, and other activities.

Since then, Star Wars Day has grown in popularity and is now celebrated by fans around the world. From movie marathons and lightsaber duels to themed parties and charity events, there is no shortage of ways for fans to express their love for the galaxy far, far away.

Global Celebrations

Star Wars Day is celebrated globally, with fans of all ages participating in a wide range of activities. In addition to organized events, many fans take to social media to share their favorite Star Wars memories, artwork, and cosplay photos using the hashtag #StarWarsDay.

In some cities, local businesses and organizations join in the celebration by offering special discounts on Star Wars merchandise or hosting themed events. Museums and theaters may also screen Star Wars films, allowing fans to experience the magic of the movies on the big screen once again.

The holiday has become a beloved tradition cherished by fans of the franchise worldwide. Whether attending organized events, hosting themed parties, or simply rewatching their favorite films at home, fans come together on May 4th to celebrate the timeless appeal of the Star Wars saga.

As the franchise continues to expand with new films, television series, books, and merchandise, the spirit of Star Wars Day remains as strong as ever, uniting fans in their shared love for a galaxy far, far away.

We focuses on the quality of your client’s accounts receivable, ignoring their financial condition.

This enables us to move quickly and fund qualified businesses including Manufacturers, Distributors and a wide variety of Service Businesses (includes SaaS) in as few as 3-5 days.

Contact me today to learn if your client is a fit.

In a widely expected decision, the Federal Open Market Committee maintained the current target range for the federal-funds rate at 5.25%-5.50 at the conclusion of a regular two-day meeting. Fed Holds Rates Steady Today.

Fed Holds Rates Steady

Policymakers have been on hold since they last raised interest rates in July 2023.

May Day, celebrated on the first day of May each year, conjures images of springtime festivities, dancing around maypoles, and an expression of workers’ rights. Yet, the origins of this globally observed day are deeply rooted in history, intertwining strands of ancient traditions, labor movements, and social upheavals. Origins of May Day.

The Origins of May Day

The earliest traces of May Day can be found in the ancient Celtic festival of Beltane. Occurring halfway between the spring equinox and the summer solstice, Beltane marked the beginning of the pastoral summer season. It was a time of fertility rituals, bonfires, and celebrations to ensure bountiful crops and livestock. The symbolism of renewal and abundance during this time echoes through the centuries, resonating in modern-day Origins of May Day festivities.

However, the modern incarnation of May Day as a day of workers’ solidarity emerged during the late 19th century. The catalyst was the struggle for the eight-hour workday, a movement that gained momentum amidst growing industrialization and labor exploitation. On May 1, 1886, hundreds of thousands of workers across the United States took to the streets in a general strike, demanding an eight-hour workday.

The culmination of this movement was the Haymarket affair in Chicago. On May 4, 1886, a peaceful rally in support of workers’ rights turned violent when a bomb was detonated, leading to casualties among both police officers and civilians. The aftermath saw a crackdown on labor activists, with several organizers, including the Haymarket martyrs, being arrested, tried, and executed.

Despite the repression, the legacy of the Haymarket affair endured, galvanizing the international labor movement. In 1889, the International Socialist Conference declared May 1 as International Workers’ Day, commemorating the struggle for the eight-hour workday and honoring the sacrifices of those who fought for labor rights.

Since then, May Day has been celebrated worldwide as a day of workers’ solidarity, marked by rallies, protests, and demonstrations advocating for better working conditions, fair wages, and social justice. Its significance transcends borders and ideologies, serving as a reminder of the ongoing struggle for workers’ rights and the collective power of organized labor.

In addition to its labor associations, May Day continues to embrace its ancient roots, with various countries incorporating traditional festivities into their celebrations. From dancing around maypoles in England to crowning the May Queen in Scandinavia, these customs serve as a testament to the enduring spirit of renewal and community that May Day embodies.

As we commemorate May Day each year, let us not only revel in its festivities but also reflect on its rich tapestry of history. From ancient rites of fertility to modern-day struggles for justice, May Day remains a symbol of resilience, solidarity, and the perennial hope for a better world.

The Assignment of Claims Act (ACA) was passed in 1940 and is codified in 31 U.S.C. § 3727 and 41 U.S.C. § 6305. The ACA allows contractors to assign their rights to receive payment from a federal contract to a third party, called an assignee, who then collects the funds from the government. The ACA’s main purpose is to help contractors and subcontractors access capital by allowing them to monetize their accounts receivable from the government. What is an Assignment of Claims?

Assignment of Claims

A contractor can assign a contract’s payments to a financing institution if the following conditions are met:

The contract is for $1,000 or more

The assignment is made to a bank, trust company, or other financing institution, including a federal lending agency

The contract doesn’t prohibit the assignment

The assignment covers all unpaid amounts unless the contract permits otherwise

The ACA also defines how lenders and factoring companies can arrange for payments when federal contracts are part of a contractor’s loans or accounts receivable. When a FACA assignment is in effect, the government is required to make contract payments directly to the designated bank or financial institution.

The reclassification of marijuana by the Biden Administration holds significant implications for the industry, influencing various aspects such as regulation, market dynamics, and societal attitudes. This article explores the effects of reclassification on these fronts and delves into potential opportunities and challenges for stakeholders.

What Reclassification of Marijuana Means to the Cannabis Industry

Regulatory Landscape: Reclassification alters the regulatory framework governing marijuana, potentially shifting it from a controlled substance to a regulated commodity. This change can lead to reforms in cultivation, distribution, and consumption laws, opening up new avenues for businesses while ensuring safety and compliance.

Market Dynamics: The reclassification of marijuana may reshape market dynamics by attracting new investors and consumers. With reduced legal barriers, businesses can expand operations, innovate products, and penetrate previously untapped markets. However, increased competition and pricing pressures may emerge as the industry matures.

Investment Opportunities: Reclassification often signals legitimacy and growth potential, attracting investments from diverse sectors. As stigma diminishes and legalization spreads, investors may flock to cannabis-related ventures, ranging from cultivation facilities to technology startups. Strategic partnerships and mergers could reshape the industry landscape, consolidating market share and fostering innovation.

Research and Development: Changes in marijuana classification facilitate research into its medical, therapeutic, and industrial applications. Expanded access to funding and resources accelerates scientific inquiry, leading to breakthroughs in treatment modalities, product formulations, and agricultural practices. Enhanced understanding of cannabinoids’ pharmacology could drive the development of novel medications and wellness products.

Social Impact: Reclassification has profound social implications, affecting public perception, criminal justice, and public health policies. Decriminalization and legalization initiatives aim to mitigate the disproportionate impact of drug enforcement on marginalized communities, fostering equity and social justice. Moreover, access to medical marijuana can improve patient outcomes and alleviate suffering, challenging misconceptions and fostering compassion.

The reclassification of marijuana represents a pivotal moment for the industry, ushering in a new era of opportunity and transformation. While uncertainties and challenges persist, stakeholders can navigate this evolving landscape by embracing innovation, collaboration, and responsible practices. By harnessing the potential of reclassification, the marijuana industry can drive positive change, benefiting individuals, communities, and economies alike.