Inflation’s Impact on Small Business

Inflation is the rate at which the general level of prices for goods and services rises, leading to a decrease in purchasing power over time. While inflation affects the entire economy, small businesses often face unique challenges when inflation rates increase. Here’s how inflation can impact small businesses: Inflation’s Impact on Small Business

1. Rising Costs of Goods and Services

One of the most direct effects of inflation on small businesses is the increase in the costs of goods and services. As prices for raw materials, inventory, and utilities rise, businesses face higher production costs. Small businesses, which often have less negotiating power and fewer bulk purchasing options than larger corporations, may struggle to absorb these increased costs without passing them on to customers.

2. Wage Pressure

Inflation often leads to higher living costs, prompting employees to demand higher wages to keep up with the increased cost of living. Small businesses may find it difficult to meet these demands, especially if their revenue does not increase at the same rate as inflation. This can lead to higher labor costs, putting additional strain on a small business’s budget.

3. Pricing Challenges

Passing on increased costs to customers through higher prices is a common response to inflation. However, this approach can be risky for small businesses, as higher prices may drive away price-sensitive customers, reducing sales volume. Small businesses must carefully balance the need to cover rising costs with the potential impact on customer demand.Inflation’s Impact on Small Business

4. Cash Flow Constraints

Inflation can disrupt cash flow, as businesses may need to pay more upfront for inventory and supplies, while customers may delay payments due to their own financial pressures. This can lead to tighter cash flow, making it difficult for small businesses to meet their obligations, such as paying suppliers, employees, or loans.

5. Interest Rate Increases

In response to inflation, central banks often raise interest rates to curb spending and bring inflation under control. Higher interest rates can increase the cost of borrowing for small businesses, making it more expensive to finance operations, expand, or invest in new opportunities. For small businesses already operating on thin margins, higher interest rates can further limit growth.

6. Changing Consumer Behavior

Inflation can change consumer behavior as people adjust their spending habits to cope with rising prices. Consumers may prioritize essential purchases and cut back on discretionary spending, which can negatively impact small businesses, especially those in industries reliant on non-essential goods and services. This shift in demand can lead to lower sales and profitability.

7. Increased Competition

As inflation pressures build, small businesses may face increased competition from larger companies that can better absorb rising costs or offer lower prices due to economies of scale. This can make it harder for small businesses to maintain their market share and attract new customers.

8. Long-Term Planning Difficulties

Inflation introduces uncertainty into the business environment, making long-term planning more difficult. Small businesses may find it challenging to set prices, forecast costs, and budget for future expenses when inflation is unpredictable. This uncertainty can lead to more conservative decision-making, potentially limiting growth and innovation.

9. Supplier Relationships

Inflation can strain relationships with suppliers, who may raise their prices or alter terms to manage their own increased costs. Small businesses may find themselves renegotiating contracts more frequently or seeking new suppliers, which can disrupt operations and add to administrative burdens.

Strategies to Mitigate Inflationary Pressures

While inflation presents significant challenges, small businesses can take steps to mitigate its impact:

- Cost Management: Focus on improving efficiency and reducing waste to keep costs under control.

- Flexible Pricing: Implement dynamic pricing strategies that allow for quick adjustments to changing costs.

- Diversification: Explore new products, services, or markets to reduce reliance on a single revenue stream.

- Supplier Negotiation: Strengthen relationships with suppliers and negotiate favorable terms to manage rising costs.

- Financial Planning: Maintain a strong cash reserve and explore fixed-rate financing options to manage cash flow and debt more effectively.

Inflation can pose significant challenges for small businesses, from rising costs to cash flow difficulties. However, by understanding these impacts and adopting proactive strategies, small businesses can navigate inflationary periods more effectively and position themselves for long-term success. Inflation’s Impact on Small Business

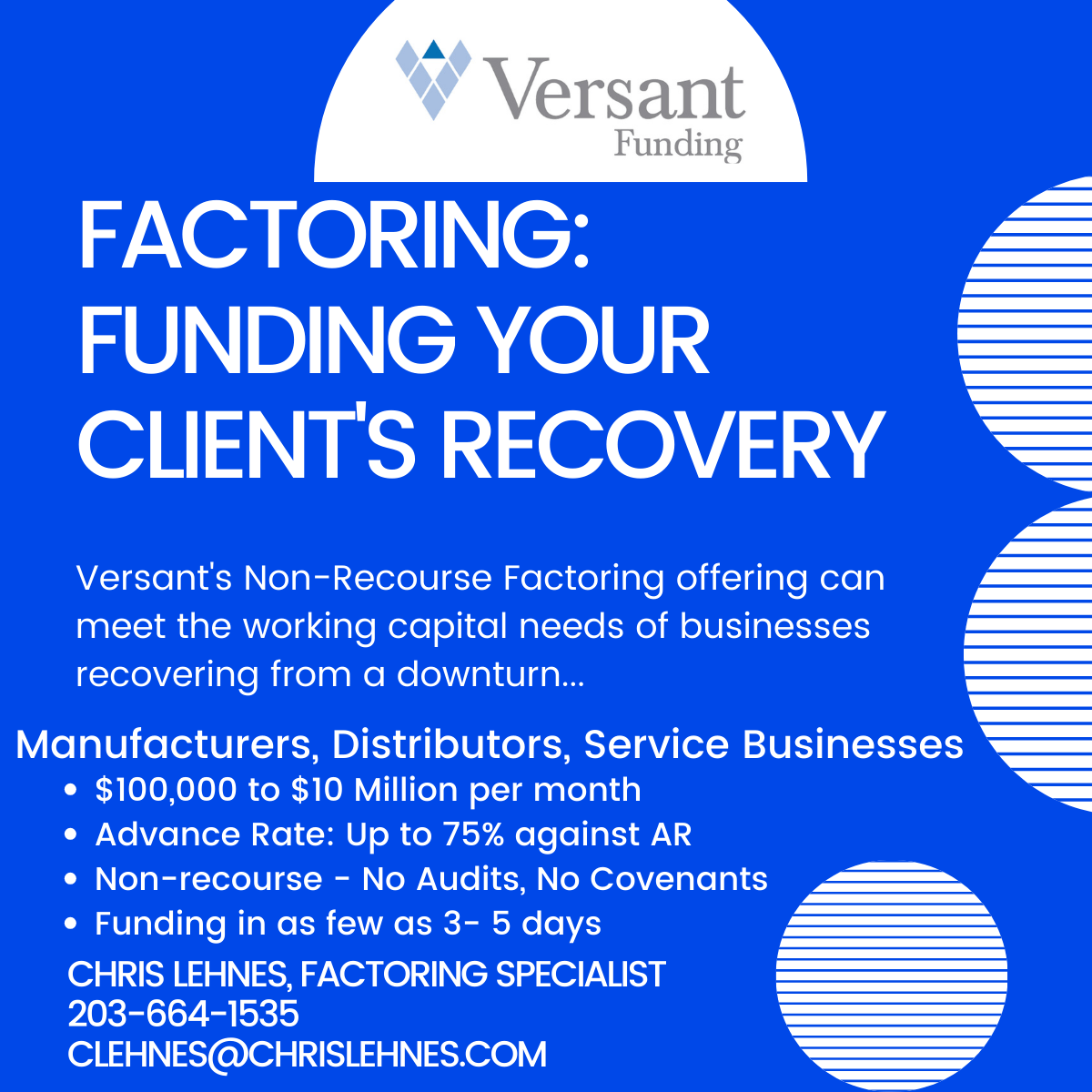

Connect with Factoring Specialist, Chris Lehnes

Inflation’s Impact on Food Prices