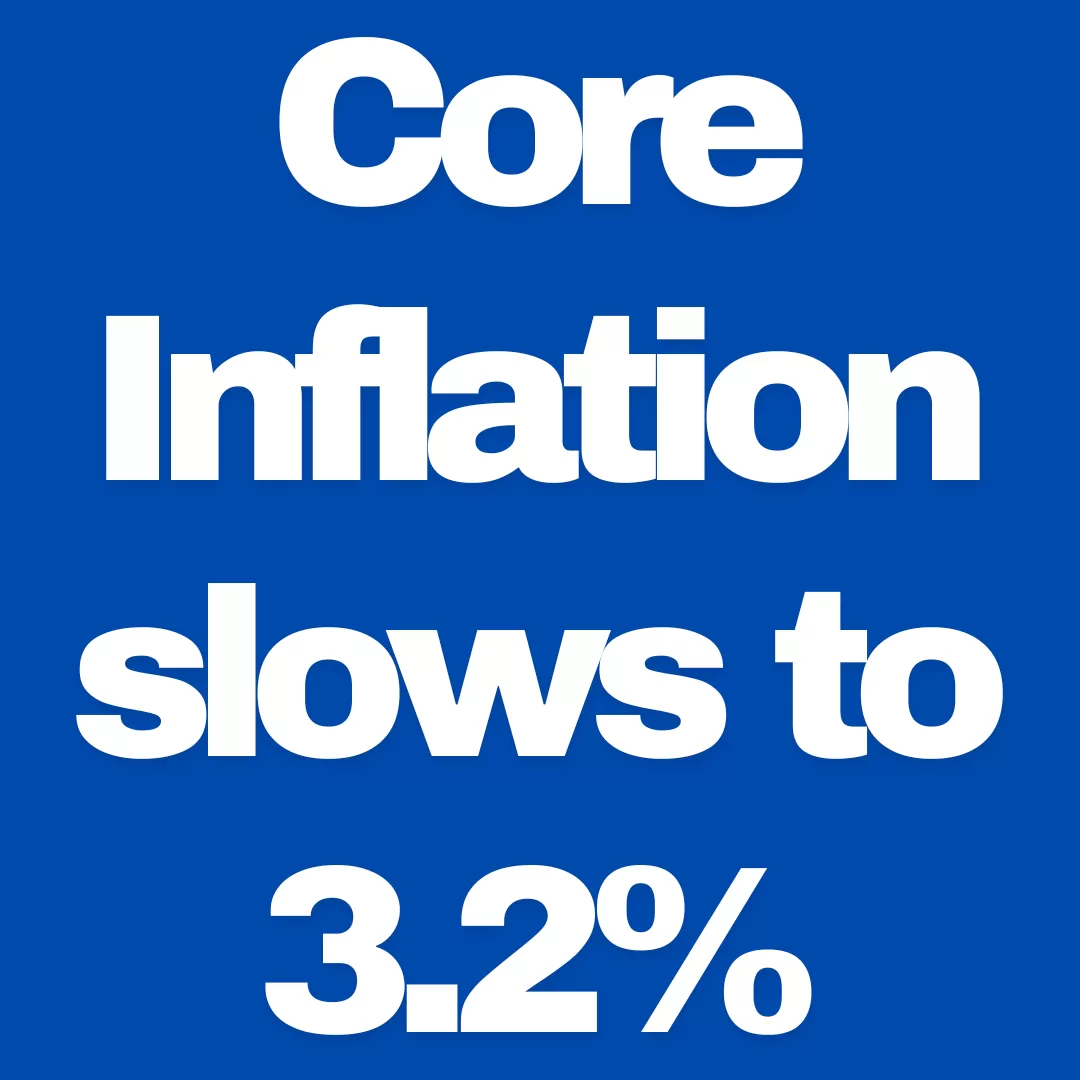

Core Inflation Slowed to 3.2% in December: Impacts and Repercussions

The U.S. economy witnessed a notable deceleration in core inflation in December, with the year-over-year rate dropping to 3.2%. This development marks a continued easing from the peak levels seen in 2022 and offers insight into the economic landscape as policymakers and consumers adapt to evolving conditions.

Understanding Core Inflation

Core inflation, which excludes volatile food and energy prices, is a critical measure for policymakers. Unlike headline inflation, it provides a clearer view of underlying price trends by eliminating short-term fluctuations. December’s figure reflects sustained progress in curbing price pressures, aided by various factors including tighter monetary policy and improving supply chain conditions.

Key Drivers of the Slowdown

- Monetary Policy Measures: The Federal Reserve’s series of interest rate hikes have played a significant role in cooling demand. Higher borrowing costs have curbed consumer spending and investment, aligning with the Fed’s objective of stabilizing inflation.

- Easing Supply Chain Bottlenecks: Improved global supply chain dynamics have helped lower production costs and increased the availability of goods. This has contributed to reduced upward pressure on prices.

- Labor Market Adjustments: While the labor market remains strong, wage growth has moderated slightly. Slower wage increases can help mitigate inflationary pressures in the services sector.

Impacts on the Economy

- Consumer Purchasing Power: Slower inflation benefits consumers by preserving purchasing power, especially for households that struggled during periods of high inflation.

- Business Outlook: Reduced inflationary pressures lower input costs for businesses, potentially leading to improved profit margins or opportunities to pass savings on to consumers.

- Policy Implications: The Federal Reserve may reassess its approach to further rate hikes. A sustained decline in inflation could pave the way for a pause or even a shift in monetary policy in the coming months.

Repercussions for Financial Markets

Financial markets have responded positively to the news, with equity indices rising and bond yields stabilizing. Investors anticipate that a slowing inflation trend may reduce the likelihood of aggressive monetary tightening, fostering a more favorable investment environment.

Risks and Uncertainties

Despite the encouraging trend, challenges remain. Core inflation is still above the Federal Reserve’s long-term target of 2%, and external factors, such as geopolitical tensions and energy price volatility, could reintroduce inflationary pressures. Additionally, the risk of a recession looms as tighter monetary policies continue to weigh on economic activity.

Looking Ahead

The deceleration in core inflation is a promising sign for economic stability. However, sustained efforts will be necessary to ensure that inflation continues its downward trajectory without triggering significant economic disruptions. Policymakers, businesses, and consumers alike must remain vigilant as the economy navigates this transitional phase.