The Federal Reserve’s recent decision to reduce interest rates by 0.25% could have nuanced effects on the U.S. economy heading into 2025, impacting areas from consumer spending to business investment. The rate cut aims to ease borrowing costs, which typically stimulates economic activity by making loans and credit more affordable. This policy shift follows a period of high interest rates intended to curb post-pandemic inflation, which has now moderated near the Fed’s 2% target. Fed Cuts Rates Again – One Quarter Point

In 2025, the lower rates are expected to encourage consumer spending and investment in sectors like housing and business expansion. Consumers may benefit from cheaper mortgage rates, which could support the housing market by making homeownership more attainable. However, savers may see reduced yields on high-interest savings accounts, as banks adjust APYs in response to the Fed’s rate cut. Fed Cuts Rates Again – One Quarter Point

The broader economic implications hinge on how inflation behaves. Some economists caution that, if economic growth remains robust and inflationary pressures resurge, the Fed might be forced to adjust its policy, which could counteract some of the benefits of lower borrowing costs. Nonetheless, many analysts view the Fed’s cautious approach as beneficial, potentially helping maintain steady growth without risking overheating the economy

The Federal Reserve is likely to cut interest rates soon as its preferred inflation measure, the Personal Consumption Expenditures (PCE) Price Index, continues to show signs of cooling. In recent months, inflation has remained modest, with the core PCE—excluding food and energy—staying stable around the Fed’s 2% target. This trend suggests that the central bank’s efforts to control inflation have been successful, and a rate cut may be imminent to further support economic growth. Fed Rate Cut is Imminent.

Fed Rate Cut Imminent Based on Its Preferred Inflation Gauge

Economists point to the Fed’s gradual success in bringing down inflation without triggering a recession as evidence that the time is right for a rate cut. The Fed has maintained high interest rates to curb inflation, but with recent data indicating that inflationary pressures are easing, the central bank may opt to lower rates to stimulate the economy. This potential move would mark a significant shift from the Fed’s earlier stance, which focused on aggressive rate hikes to combat rising prices.Fed Rate Cut is Imminent

Consumer spending has shown resilience despite the cooling inflation, further supporting the case for a rate cut. The Fed’s decision will likely depend on upcoming economic data, but the consistent downward trend in inflation suggests that the central bank is nearing the point where it can confidently reduce rates. This anticipated move is expected to be announced in the coming months, possibly as early as the Fed’s next meeting. Fed Rate Cut is Imminent

As the Fed navigates this delicate balance between controlling inflation and fostering economic growth, the financial markets and broader economy are closely watching for signs of the first rate cut in this cycle. A reduction in rates could provide a boost to both consumer confidence and business investment, helping to sustain the economic expansion while keeping inflation in check. Fed Rate Cut is Imminent.

Time has come – Powell Confirms Rate Cuts are Imminent

Federal Reserve Chair Jerome Powell’s announcement that “the time has come” for rate cuts marks a pivotal moment in the U.S. economic cycle. This decision, coming after a period of sustained interest rate hikes, signals a significant shift in the Federal Reserve’s monetary policy strategy. The declaration is likely a response to evolving economic conditions, including slowing growth, easing inflation pressures, and rising concerns about global economic stability. This article will explore the implications of this policy shift, the economic factors driving the decision, and potential outcomes for various sectors of the economy.

1. The Economic Backdrop: Why Rate Cuts Now?

Over the past few years, the Federal Reserve had pursued a series of rate hikes to combat rising inflation and prevent the economy from overheating. However, recent economic indicators suggest that the tide is turning. Key factors likely influencing Powell’s decision include:

Slowing Economic Growth: GDP growth has shown signs of deceleration, with consumer spending and business investment softening. This slowdown may have prompted the Fed to consider rate cuts as a preemptive measure to avoid a recession.

Easing Inflation Pressures: After a period of elevated inflation, recent data may show that price pressures are beginning to ease, reducing the need for restrictive monetary policy.

Global Economic Uncertainty: Ongoing geopolitical tensions, supply chain disruptions, and slowing growth in major economies like China and Europe could have added to the Fed’s concerns about global economic stability. Time has come.

2. The Impact of Rate Cuts on the U.S. Economy

The decision to cut rates will have wide-ranging effects across the economy. Some potential impacts include:

Stimulating Consumer Spending and Investment: Lower interest rates reduce the cost of borrowing, encouraging consumers and businesses to take out loans for spending and investment. This can help boost demand and support economic growth.

Housing Market Revival: The housing market, which is sensitive to interest rates, could see a revival as lower mortgage rates make home purchases more affordable. This could lead to increased home sales and construction activity.

Financial Markets Reaction: Financial markets often react positively to rate cuts, as lower rates can boost corporate profits and make equities more attractive relative to bonds. However, if the rate cuts are perceived as a sign of deeper economic troubles, market volatility could increase. Time has come.

3. Risks and Challenges: Is the Timing Right?

While rate cuts can provide a much-needed boost to the economy, they are not without risks:

Inflationary Pressures: If the economy rebounds too quickly, or if inflation has not fully abated, cutting rates could reignite inflationary pressures, forcing the Fed to reverse course quickly.

Asset Bubbles: Prolonged low-interest rates can lead to excessive risk-taking in financial markets, potentially inflating asset bubbles that could burst and lead to financial instability.

Diminished Policy Tools: With rates already low, further cuts leave the Fed with less room to maneuver in the event of a more severe economic downturn.

4. The Global Context: How Will Other Central Banks Respond?

The Federal Reserve’s move to cut rates will have global repercussions. Other central banks, particularly in Europe and Asia, may face pressure to follow suit to prevent capital outflows and maintain competitive exchange rates. The coordination (or lack thereof) among central banks could influence global financial stability and economic performance.

5. Looking Ahead: What to Expect in the Coming Months

The immediate aftermath of Powell’s announcement will likely include increased market speculation about the pace and magnitude of future rate cuts. The Fed’s communication strategy will be crucial in managing expectations and preventing market overreaction. Key indicators to watch include:

Future Fed Statements and Economic Projections: Any hints about the Fed’s longer-term view on rates will be closely scrutinized by investors and economists.

Economic Data Releases: Upcoming data on inflation, employment, and GDP will play a critical role in shaping the Fed’s actions and market expectations.

Conclusion:

Jerome Powell’s declaration that “the time has come” for rate cuts represents a turning point in U.S. monetary policy. While the move is likely aimed at sustaining economic growth in the face of rising uncertainties, it also carries risks that must be carefully managed. The Federal Reserve’s ability to navigate this delicate balancing act will be crucial in determining the trajectory of the U.S. and global economies in the coming years. As always, the Fed’s actions will be closely watched, with profound implications for markets, businesses, and consumers alike.

The Federal Reserve has recently indicated a possible interest rate cut in September, responding to signs of slowing economic growth and rising global uncertainties. This potential move marks a significant shift in the Fed’s policy, aimed at sustaining the longest economic expansion in U.S. history.

Key Points:

Economic Indicators:

Recent data suggest a slowdown in U.S. manufacturing and business investment.

Consumer spending remains strong, but there are concerns about the impact of trade tensions and global economic slowdown.

Global Economic Concerns:

The ongoing trade war between the U.S. and China has created uncertainty in global markets.

Slowing growth in major economies like China and Europe adds to the cautious outlook.

Market Reactions:

Financial markets have responded positively to the possibility of a rate cut.

Stock indices have seen gains, reflecting investor optimism.

Federal Reserve’s Position:

Fed Chairman Jerome Powell emphasized the central bank’s commitment to act as appropriate to sustain the expansion.

The Fed is closely monitoring economic data and global developments to guide its decisions.

Potential Impact:

A rate cut could lower borrowing costs, encouraging investment and spending.

It might also help mitigate the risks posed by global uncertainties and trade tensions.

The Federal Reserve’s indication of a potential rate cut in September highlights its proactive approach in addressing economic challenges and supporting continued growth. The decision will ultimately depend on upcoming economic data and developments in global trade.

On June 12, 2024, the Federal Reserve announced that it would keep interest rates unchanged. This decision comes amid ongoing assessments of economic conditions, including inflation, employment rates, and overall economic growth. By maintaining the current interest rates, the Fed aims to balance fostering economic growth while keeping inflation in check.

Fed Keeps Rates Unchanged

Key Points:

Interest Rates: The Federal Reserve decided to maintain the current interest rates, signaling a steady approach to monetary policy.

Economic Conditions: The decision reflects the Fed’s view on current economic indicators such as inflation, employment, and GDP growth.

Future Outlook: The Fed will continue to monitor economic data and make adjustments as necessary to support its dual mandate of maximum employment and price stability.

Implications:

For Consumers: Borrowing costs, including mortgage rates and credit card interest rates, are likely to remain stable in the short term.

For Businesses: Stability in interest rates can help businesses plan for investments and expansions with greater certainty.

For Investors: The stock market may react to the news with adjustments based on expectations for future economic conditions.

This decision underscores the Federal Reserve’s cautious approach in navigating the complex economic landscape post-pandemic, ensuring that any policy changes are well-grounded in the prevailing economic realities.

For several years, economic analysts and commentators have been sounding alarms about an impending recession. However, despite these warnings, the anticipated economic downturn has yet to occur. This phenomenon has puzzled experts and prompted a deeper analysis of the underlying factors that have contributed to the economy’s resilience. Several key reasons can be identified for the failure of the long-predicted recession to materialize.

1. Strong Consumer Spending

One of the most significant drivers of economic growth is consumer spending. Over the past few years, consumer confidence has remained robust, bolstered by low unemployment rates, rising wages, and substantial savings accumulated during the pandemic. Even amid inflationary pressures, consumers have continued to spend, fueling demand for goods and services and keeping the economy buoyant.

2. Labor Market Resilience

The labor market has shown remarkable strength, with unemployment rates at historic lows and job creation consistently outpacing expectations. This tight labor market has led to wage growth, which, in turn, has supported consumer spending. Furthermore, many sectors have adapted to new ways of working, such as remote and hybrid models, which have enhanced productivity and efficiency.

3. Government Fiscal Policies

Government intervention through fiscal policies has played a crucial role in stabilizing the economy. Stimulus packages, unemployment benefits, and other support measures implemented during the pandemic have provided a safety net for businesses and individuals. Additionally, infrastructure investments and other government spending initiatives have spurred economic activity and job creation.

4. Monetary Policy Adaptability

Central banks, particularly the Federal Reserve in the United States, have demonstrated adaptability in their monetary policies. By carefully managing interest rates and employing quantitative easing measures, central banks have maintained liquidity in the financial system and kept borrowing costs low. This has encouraged investment and spending, preventing the economy from sliding into recession.

5. Corporate Adaptation and Innovation

Businesses have shown remarkable adaptability and innovation in response to changing economic conditions. The pandemic accelerated digital transformation across industries, leading to increased efficiency and the creation of new business models. Companies that embraced technology and adapted their operations have not only survived but thrived, contributing to overall economic stability.

6. Global Economic Dynamics

The global economy has also played a role in mitigating recession risks. Strong economic performance in major economies, such as China and the European Union, has provided a boost to global trade and investment. Moreover, global supply chain disruptions, while challenging, have led to increased domestic production and sourcing, fostering economic resilience.

7. Stock Market Performance

Despite periodic volatility, stock markets have generally performed well, reflecting investor confidence in the economy. High valuations in equity markets have supported consumer and business wealth, further reinforcing economic stability. Additionally, the availability of capital through financial markets has enabled companies to invest in growth and innovation.

8. Sectoral Shifts and Diversification

The economy has witnessed significant sectoral shifts and diversification, with growth in areas such as technology, healthcare, and renewable energy offsetting weaknesses in traditional industries. This diversification has reduced the overall economic vulnerability to sector-specific downturns, contributing to sustained growth.

Conclusion

The anticipated recession has failed to materialize due to a combination of strong consumer spending, a resilient labor market, effective government policies, adaptable monetary strategies, corporate innovation, supportive global economic dynamics, robust stock market performance, and sectoral diversification. While the future remains uncertain and potential risks persist, these factors have collectively supported the economy and prevented the long-predicted downturn. As the economic landscape continues to evolve, ongoing vigilance and adaptability will be essential to maintaining stability and growth.

Food companies continue to struggle with the lingering impacts of inflation, even as general inflation rates have begun to decline. The reasons behind persistent high food prices are multifaceted, encompassing supply chain disruptions, increased production costs, and corporate profit strategies.

Inflation’s Impact on Food Companies

Despite a decrease in overall inflation, food prices remain elevated due to a combination of factors such as higher costs for labor, transportation, and raw materials. For example, the cost of energy, which surged during the COVID-19 pandemic and was further exacerbated by geopolitical events like the Russian invasion of Ukraine, significantly impacted food production costs. This spike in energy prices led to increased costs for fertilizers and other agricultural inputs, driving up the prices of both processed and unprocessed foods (European Central Bank) (Northeastern Global News).

Moreover, many food companies have taken advantage of inflationary pressures to enhance their profit margins. Corporations like Tyson Foods and Kroger have reported substantial profit increases through price hikes that exceed their rising costs, suggesting a degree of price manipulation. This practice is evident in instances where companies have also engaged in significant stock buybacks and dividend increases, benefiting shareholders at the expense of consumers (Jacobin).

Consumers are acutely feeling these effects, with grocery prices remaining high and eating out becoming more expensive. For instance, food prices in supermarkets are now about 25% higher than in January 2020, which is above the overall inflation increase of 19% during the same period (Northeastern Global News). This sustained price elevation in essential goods has put a strain on household budgets, particularly impacting lower-income families.

In summary, the high food prices seen today are a result of complex and interrelated factors, including lingering supply chain issues, increased production costs, and strategic corporate behaviors aimed at maximizing profits. These elements collectively ensure that food companies, and by extension consumers, continue to bear the financial burden of past inflationary periods (Jacobin) (BNN).

Few metrics hold as much sway and significance as interest rates. From impacting borrowing costs to influencing investment decisions, fluctuations in interest rates can reverberate throughout the global economy. Chief Financial Officers (CFOs) are key figures in navigating these dynamics, as their insights and strategies shape how businesses respond to changing interest rate environments. In this article, we delve into the perspectives of CFOs regarding the direction of interest rates, exploring their sentiments, predictions, and the implications for corporate decision-making.

CFOs Speak Out on Interest Rates

Understanding the Significance of Interest Rates: Interest rates serve as a fundamental mechanism for regulating economic activity. Central banks adjust interest rates to manage inflation, stimulate economic growth, or curb excessive borrowing. For businesses, interest rates directly influence the cost of capital, impacting investment decisions, capital expenditures, and overall financial health.

Insights from CFO Surveys: Numerous surveys and studies regularly gauge the sentiments of CFOs regarding interest rate trends. These surveys provide valuable insights into how finance leaders perceive the trajectory of interest rates and the potential implications for their organizations.

Optimism Amidst Uncertainty: CFO sentiment towards interest rates often reflects broader economic outlooks. During periods of economic expansion and stability, CFOs may express confidence in a gradual increase in interest rates, signaling robust growth prospects. Conversely, economic uncertainty or recessionary concerns may lead CFOs to anticipate rate cuts or prolonged low rates to stimulate economic activity.

Impact on Financing Decisions: Interest rate forecasts significantly influence corporate financing decisions. CFOs must weigh the benefits of accessing capital at lower rates against the potential risks of rising borrowing costs. For instance, in a low-interest-rate environment, companies may pursue debt financing for expansion projects or strategic acquisitions. Conversely, rising interest rates may prompt a shift towards equity financing or tighter capital expenditure controls to manage financial risk.

Hedging Strategies and Risk Management: CFOs employ various hedging strategies to mitigate the impact of interest rate fluctuations on their organizations. Interest rate swaps, options, and other derivative instruments enable companies to lock in favorable rates or protect against adverse movements. These risk management tactics are essential for safeguarding financial stability and ensuring resilience against volatile market conditions.

Global Macroeconomic Factors: Interest rate trends are influenced by a complex interplay of global macroeconomic factors, including geopolitical events, monetary policy decisions, and inflationary pressures. CFOs must closely monitor these developments and adapt their strategies accordingly to navigate evolving market dynamics and mitigate potential risks to their businesses.

In an ever-changing economic landscape, CFOs play a pivotal role in interpreting and responding to interest rate trends. By staying attuned to market signals, leveraging financial instruments, and implementing prudent risk management practices, CFOs can steer their organizations through uncertain times and capitalize on opportunities for sustainable growth and value creation. As interest rates continue to evolve, CFOs will remain vigilant, ensuring that their organizations remain agile and resilient in the face of economic uncertainty.

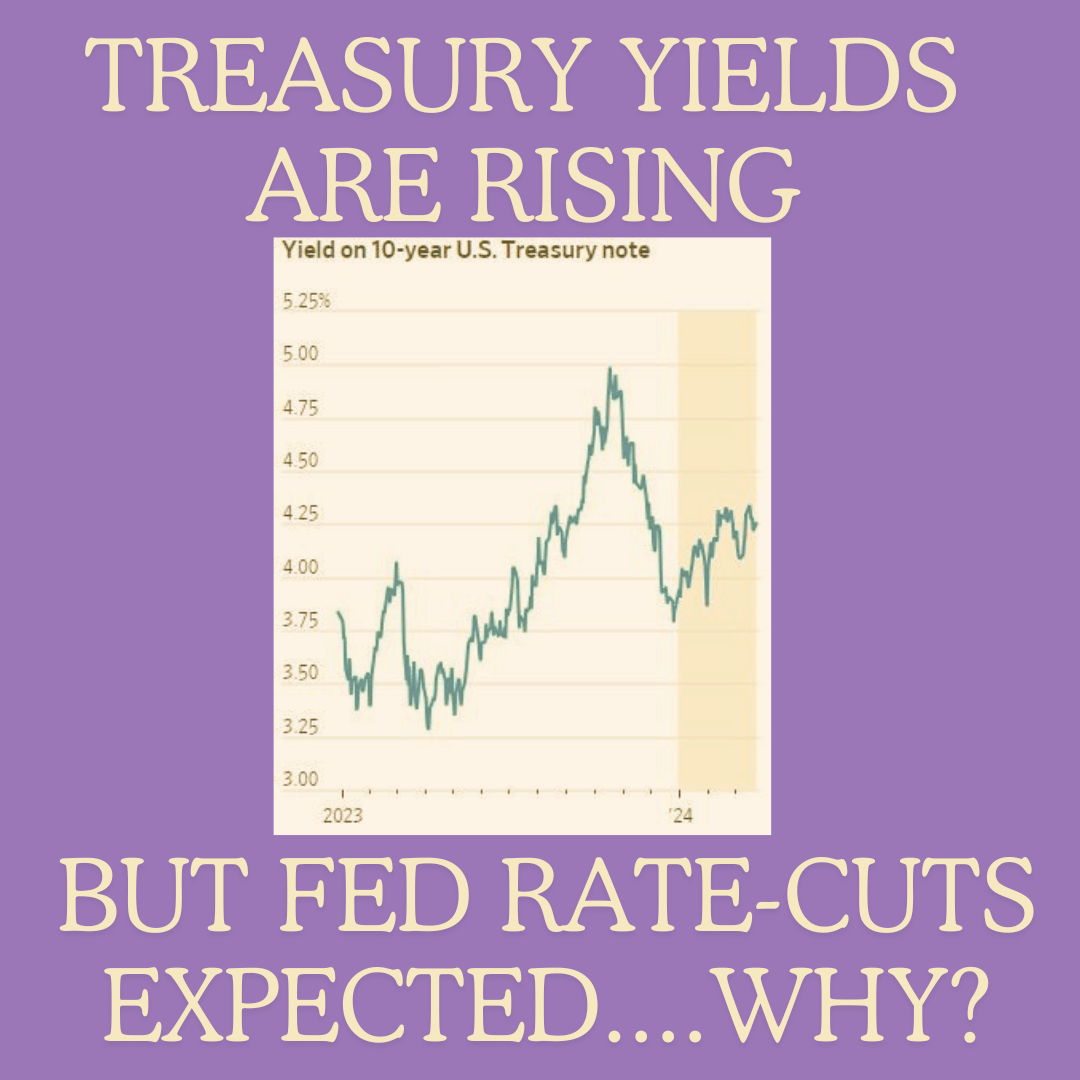

In the intricate dance of financial markets, certain phenomena can sometimes seem counterintuitive. One such puzzle currently perplexing investors is the simultaneous rise in Treasury yields alongside expectations of interest rate cuts by the Federal Reserve. While conventional wisdom might suggest that falling interest rates would naturally lead to lower yields on government bonds, the reality is often more nuanced. In this article, we delve into the factors driving this divergence and explore its implications for investors and the broader economy.

1. The Role of Market Expectations

At the heart of this conundrum lies the delicate interplay between market expectations and economic fundamentals. When investors anticipate a future reduction in interest rates by the Federal Reserve, they adjust their investment strategies accordingly. This can manifest in increased demand for Treasury securities, particularly longer-dated bonds, as investors seek to lock in higher yields before rates potentially decline further. Consequently, this surge in demand exerts upward pressure on bond prices and drives yields lower.

2. Inflationary Concerns

However, the picture becomes more complex when inflationary pressures enter the equation. Inflation erodes the real value of fixed-income investments such as bonds, leading investors to demand higher yields as compensation for the diminished purchasing power of future cash flows. In recent times, mounting concerns about inflation, fueled by supply chain disruptions, robust consumer demand, and fiscal stimulus measures, have contributed to upward pressure on Treasury yields.

3. Economic Growth Expectations

Moreover, rising Treasury yields can also reflect optimism about the economic outlook. When investors anticipate robust economic growth, they often rotate out of safe-haven assets like government bonds and into riskier investments such as equities. This shift in sentiment can drive up Treasury yields as bond prices fall in response to reduced demand. Hence, the prospect of Fed rate cuts may be outweighed by bullish sentiment regarding the broader economic landscape, prompting investors to demand higher yields on Treasury securities.

4. Yield Curve Dynamics

Another crucial aspect to consider is the shape of the yield curve. In a normal economic environment, longer-dated Treasury yields are higher than shorter-dated ones to compensate investors for the increased risk associated with holding bonds over a more extended period. However, when short-term interest rates are expected to decline, the yield curve may flatten or even invert as investors anticipate a slowing economy and lower future returns. In such scenarios, longer-dated Treasury yields could rise despite expectations of Fed rate cuts.

Implications for Investors and the Economy

For investors, navigating this environment requires a nuanced understanding of the interplay between monetary policy, inflation dynamics, and economic fundamentals. While rising Treasury yields may present opportunities for those seeking higher returns, they also entail heightened risks, particularly in a potentially inflationary environment.

From a broader economic perspective, the divergence between rising Treasury yields and anticipated Fed rate cuts underscores the complexity of policymaking in an uncertain environment. The Federal Reserve must carefully balance its dual mandate of promoting maximum employment and stable prices while responding to evolving market conditions.

In conclusion, the current phenomenon of rising Treasury yields amidst expectations of Fed rate cuts underscores the multifaceted nature of financial markets. Investors and policymakers alike must remain vigilant in assessing the myriad factors driving market dynamics and their implications for the economy at large. By staying informed and adaptable, stakeholders can navigate this challenging landscape with greater confidence and resilience.

Interest Rates: Navigating the Highs and Lows: In the world of finance, interest rates are the heartbeat of economic activity. They dictate the cost of borrowing and the return on investments, influencing everything from consumer spending to business expansion. However, the story of interest rates is one of perpetual fluctuation, often oscillating between two extremes: too high and too low.

The Highs: Challenges and Opportunities

When interest rates soar to lofty heights, businesses face a myriad of challenges. For starters, the cost of borrowing increases, making it more expensive for companies to finance new projects or expand their operations. Small businesses, in particular, may find themselves struggling to access affordable credit, hindering their growth potential.

Moreover, high interest rates can dampen consumer spending as the cost of loans, such as mortgages and car loans, becomes prohibitive. This reduction in consumer demand can have ripple effects across various industries, leading to decreased sales and revenue for businesses.

However, amidst the challenges, there are also opportunities to be found in high-interest-rate environments. Savvy investors may capitalize on higher returns from fixed-income securities such as bonds, as interest payments increase along with rates. Additionally, businesses with strong cash reserves may leverage their financial stability to acquire distressed assets or invest in growth opportunities during economic downturns, when interest rates typically rise.

The Lows: Stimulus and Risk

Conversely, when interest rates plummet to historic lows, businesses encounter a different set of circumstances. While low rates can stimulate economic activity by encouraging borrowing and spending, they also introduce unique risks and complexities.

For instance, in a low-interest-rate environment, the cost of borrowing becomes significantly cheaper, incentivizing businesses to take on debt to fuel expansion or fund acquisitions. While this may stimulate short-term growth, it can also lead to overleveraging and financial instability if not managed prudently.

Moreover, low interest rates can distort asset prices, inflating valuations across equity markets and real estate sectors. This phenomenon, commonly referred to as the “search for yield,” can create speculative bubbles that pose systemic risks to the financial system.

Despite these risks, low interest rates present compelling opportunities for businesses seeking to optimize their capital structure. Companies can refinance existing debt at more favorable terms, reducing interest expenses and improving cash flow. Additionally, businesses may explore innovative financing solutions, such as issuing bonds or accessing alternative lending platforms, to capitalize on low-cost capital.

Navigating the Highs and Lows: A Strategic Approach

In an environment where interest rates are both too high and too low, businesses must adopt a strategic approach to navigate the complexities of the financial landscape. This entails:

Risk Management: Proactively assess and mitigate risks associated with interest rate fluctuations, including exposure to variable-rate debt and interest rate derivatives.

Capital Allocation: Evaluate investment opportunities based on their risk-adjusted returns and alignment with long-term strategic objectives, considering the impact of interest rates on financing costs and investment returns.

Financial Flexibility: Maintain a flexible capital structure that enables agility in response to changing market conditions, including access to diverse sources of funding and liquidity buffers to withstand economic shocks.

Continuous Monitoring: Stay informed about macroeconomic trends, central bank policies, and geopolitical developments that may influence interest rates and financial markets, adjusting business strategies accordingly.

In conclusion, the story of interest rates is one of complexity and nuance, characterized by alternating periods of highs and lows. While each extreme presents its own set of challenges and opportunities, businesses that embrace a strategic and adaptive approach can navigate the highs and lows of interest rates with resilience and success.