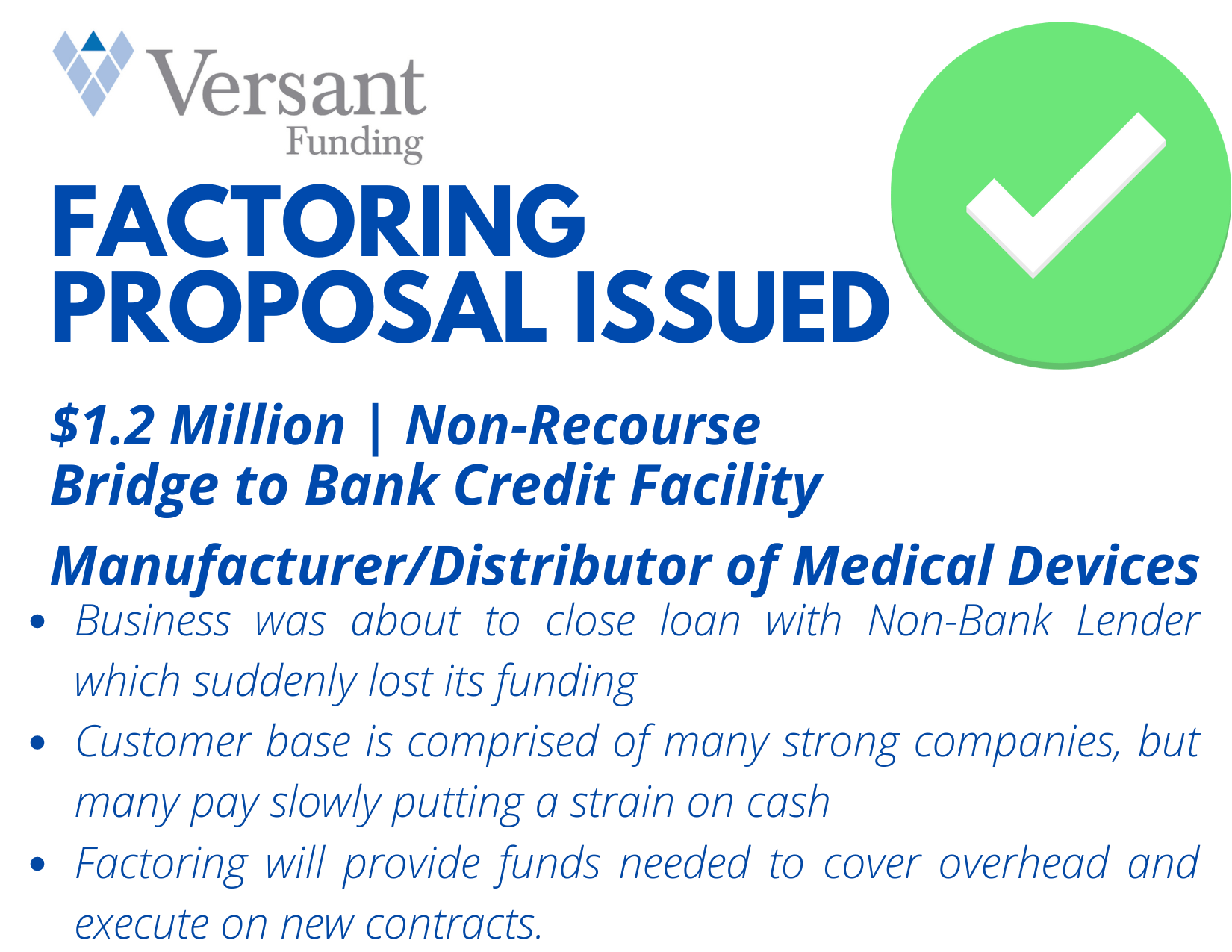

Factoring Proposal Accepted| $2.5 Million| Service Provider

Factoring Proposal Accepted| $2.5 Million| Service Provider

Accounts receivable factoring involves a process where a business sells its accounts receivable (invoices) to a third-party financial company (factor) at a discount. The factor then collects payments from the customers on those invoices. Here’s how the notification and verification process typically works:

Overall, the notification and verification process in accounts receivable factoring is crucial for ensuring transparency, accuracy, and efficiency in managing the financing of invoices and collecting payments from customers. It involves close coordination between the factor, the business, and its customers to facilitate smooth transactions and minimize the risk of disputes or payment delays.

Factoring offering can quickly fund Service Providers (as well as Manufacturers and Distributors) which do not meet traditional lending standards but have good quality accounts receivable outstanding.

Program Overview

Think of me for Consultants, Staffing Companies or SaaS clients which need cash to meet their immediate goals.

Contact me at 203-664-1535 or clehnes@chrislehnes.com

Connect with Factoring Specialist, Chris Lehnes on LinkedIn

Connect with Factoring Specialist, Chris Lehnes on LinkedIn

Learn about other factoring proposals issued

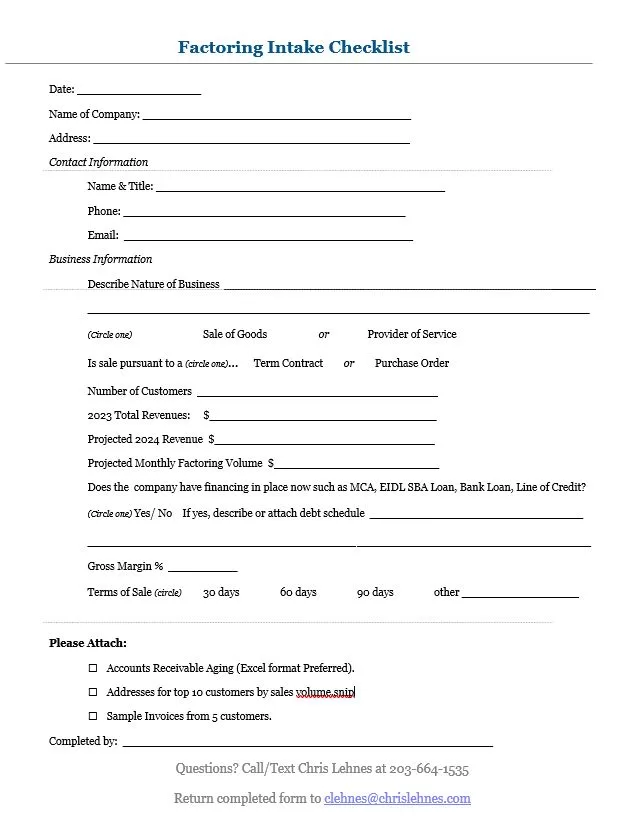

Intake Checklist:

In the realm of business financing, entrepreneurs are continually seeking innovative strategies to fuel growth and expansion. One such method gaining traction is accounts receivable factoring, a financial tool that allows companies to leverage their outstanding invoices to secure immediate cash flow. By unlocking the value of their accounts receivable, businesses can access working capital quickly and efficiently, facilitating growth initiatives and seizing new opportunities. So, how does accounts receivable factoring work, and what are the benefits it offers for businesses aiming to scale up?

Accounts receivable factoring, also known as invoice factoring, involves a third-party financial institution, known as a factor, purchasing a company’s outstanding invoices at a discount. Instead of waiting for customers to pay their invoices on their usual terms, the business receives an immediate cash advance from the factor, typically ranging from 70% to 90% of the invoice value. The factor then assumes responsibility for collecting payments from the customers. Once the invoices are paid, the factor remits the remaining balance to the business, minus a fee for their services.

Accounts receivable factoring offers businesses a flexible and scalable financing solution to support growth initiatives. By converting outstanding invoices into immediate cash flow, companies can seize opportunities for expansion, such as launching new products or services, investing in marketing campaigns, or expanding their operations. Unlike traditional loans, which may involve lengthy approval processes and stringent credit checks, factoring provides rapid access to capital without adding debt to the balance sheet.

For businesses grappling with cash flow challenges, accounts receivable factoring provides a reliable mechanism to maintain liquidity and meet financial obligations. By accelerating the collection of receivables, companies can alleviate cash flow gaps and ensure steady operations. This liquidity cushion enables businesses to navigate seasonal fluctuations, cover operational expenses, and pursue growth opportunities with confidence.

Accounts receivable factoring can also bolster a company’s creditworthiness by improving its cash flow metrics. By converting receivables into cash, businesses reduce their reliance on traditional forms of financing, such as loans or lines of credit. This can enhance their financial profile and position them more favorably when seeking additional funding from lenders or investors. Moreover, since factoring is based on the creditworthiness of customers rather than the business itself, it can be an accessible financing option for companies with limited credit history or poor credit scores.

Accounts receivable factoring represents a powerful tool for businesses seeking to fuel growth and navigate financial challenges. By converting outstanding invoices into immediate cash flow, companies can unlock capital to invest in expansion initiatives, improve cash flow management, and enhance their creditworthiness. As businesses continue to adapt to evolving market dynamics and pursue ambitious growth strategies, accounts receivable factoring offers a flexible and accessible financing solution to support their objectives.

Versant Funding worked with a software company in the Midwest to provide a non-recourse spot factoring transaction in support of the company’s sale to a private equity group. Chris Lehnes, a business development officer for Versant Funding, explained the intricacies of the deal as well as the benefits of and uses for spot factoring more generally.

How was this financing opportunity originated? Was it through organic business development or referral?

The investment banker representing this business on a pending sale to a private equity group was first introduced to me several years ago. He’s been in my marketing database ever since and called after receiving one of my email marketing campaigns with what he thought was a “crazy idea” of using factoring to meet his client’s urgent working capital needs.

Why did the company need financing and why was a non-recourse spot factoring facility the right option?

The company was a couple of weeks from closing on the sale of their business, but one of the conditions of closing was the seller meeting certain obligations that the business did not have the cash on hand to accomplish. The deadline to meet one of these obligations was about a week away, so a speedy funding solution was essential.

With our non-recourse factoring program, we rely solely on the strength of our client’s customers. Therefore, we did not need to spend time underwriting the business and getting comfortable with their performance. They had an invoice outstanding from a large, multinational food business with a very strong credit rating which was expected to pay in a couple of weeks. Factoring this one invoice would provide the business the cash they required to meet their obligation and our quick process was able to meet their very short time frame.

What were some of the unique elements of this deal, if any?

Versant Funding’s preference is to enter into ongoing factoring relationships with our clients, so the simple fact that we were providing “spot” factoring made the transaction somewhat unique for us. But, in addition, the company had a tax lien with a payment plan in place. Since there were insufficient proceeds to pay off this lien, we escrowed a few months of payments, which provided us protection against the company falling behind on their payments before we were paid by their account debtor.

The client in this deal was in the process of completing a sale to a private equity group. How did the ongoing sale process affect this deal, if at all?

The impending sale kept the client highly motivated to close the deal promptly and very responsive to our requests along the path to a quick funding.

How does non-recourse spot factoring differ from other types of factoring arrangements?

While many factors require an ongoing factoring commitment, our willingness to fund spot transactions enables us to also fund businesses which have a very short-term working capital need which can be met by factoring a single invoice.

The non-recourse aspect of our factoring program allows us to fund “tough” transactions that would be declined by most recourse factors. Since we are solely focused on the strength of our clients’ customers, the financial performance of our clients is not relevant to us. That enables us to fund businesses that are very new, growing rapidly or struggling as long as those businesses have strong customers and therefore good quality accounts receivable. Recourse factors are typically underwriting the performance of the business and the strength of management as well as the quality of the A/R. Many of our non-recourse factoring clients either would not pass that scrutiny or simply do not have the time to wait for the underwriting process to be completed.

What kind of demand has Versant Funding seen for spot factoring facilities like this during the first half of 2021? Are you expecting more or less activity on the spot factoring front as the year goes on?

Recently, I have seen an increase in spot factoring requests as compared to prior years. However, in at least one case, while the initial request was for spot factoring, after further discussions of the benefits of an ongoing factoring arrangement, the client accepted our proposal for a 24-month factoring facility.

I am constantly marketing to my referral sources how Versant Funding’s non-recourse factoring program can be used as a bridge. Often, we are providing a bridge to an equity raise or a sale or just providing a company time to grow and stabilize to the point that they can qualify for bank financing, which could be years away. I expect that my messaging will continue to also source short-term bridge opportunities where a spot factoring arrangement may be a better fit.

Q&A – Chris Lehnes Discusses Spot Factoring

Video – Factoring: The Solution to your Working Capital Problems

For more information contact Chris Lehnes | 203-664-1535 | clehnes@chrislehnes.com

Latest Factoring Proposal Accepted: $400k – Non Recourse