Inflation Hits 2.6% in October, Meeting Expectations

In October, the inflation rate rose to 2.6%, aligning with analysts’ forecasts. This increase reflects a steady trend as energy costs, housing prices, and some core services continued to drive up consumer prices. The 2.6% rise marks a moderate increase from previous months, where inflation had shown signs of slowing, but remains below the peaks seen earlier in the year. Inflation increases to 2.60%.

Key Drivers Behind the Inflation Rise

The primary contributors to October’s inflation increase were:

Energy Costs: Fuel and utility costs climbed again, adding pressure to household budgets and affecting goods transportation.

Housing Costs: The ongoing rise in rental and housing prices continued to drive inflation, as demand for housing remains robust.

Core Services: Services like healthcare, insurance, and education also saw incremental price increases, contributing to the overall inflation rate.

Implications for the Economy

While the inflation rate is still within a manageable range, it remains above central banks’ typical target of 2%. This could prompt monetary policymakers to consider further adjustments to interest rates if inflation persists. For consumers, continued inflation might influence spending behaviors, especially in discretionary spending areas, as they navigate higher living costs.

Analysts are closely watching future data to see if this trend holds or if the economy will see further moderation in inflation in response to central bank policies and global economic conditions.

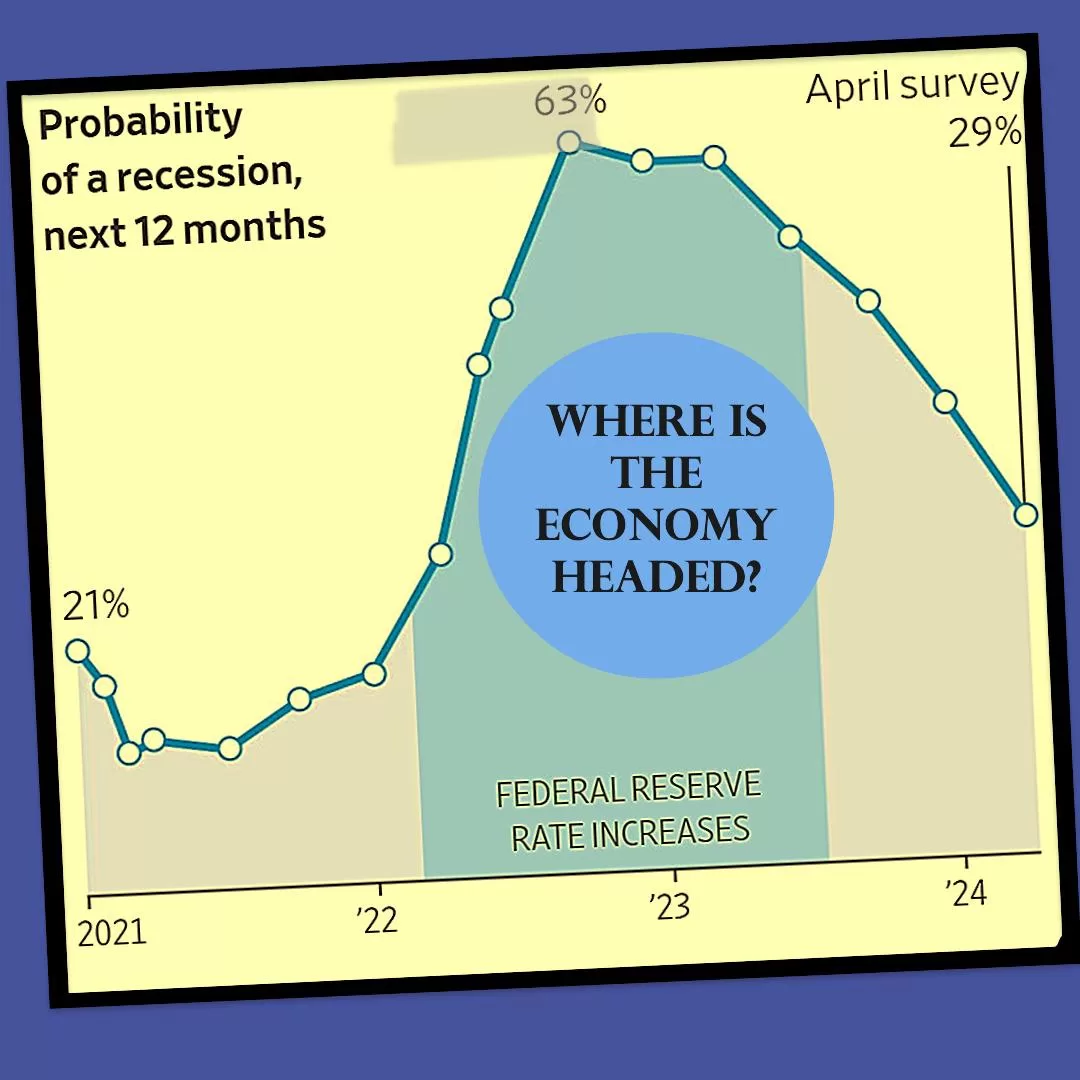

Immigration can contribute to economic growth by expanding the labor force, increasing productivity, and driving innovation. Immigrants often fill essential roles in industries experiencing labor shortages, helping to sustain and grow businesses. Where is the Economy Headed in 2024?

Where is the Economy Headed in 2024?

Consumer spending is a critical driver of economic growth, as it accounts for a significant portion of overall economic activity. When consumers feel confident about their financial situation and job prospects, they are more likely to spend on discretionary items, leading to increased demand and economic expansion. Where is the Economy Headed in 2024?

Given the robust growth fueled by these factors, economists are optimistic about the economy’s near-term outlook. Confidence in job security is likely bolstering consumer sentiment, encouraging continued spending and economic momentum. As a result, economists don’t foresee the economy entering a recession in the coming year.

It’s important to monitor various economic indicators and external factors to assess the sustainability of this growth trajectory and identify any potential risks or challenges that may arise in the future.

The job gains surpassing forecasts indicate a robust labor market, potentially buoyed by factors such as increased immigration contributing to population growth. A growing population can create additional demand for goods and services, which in turn stimulates job creation across various sectors of the economy.

However, economists’ anticipation of an imminent slowdown suggests that there are constraints on the labor market’s ability to sustain this rapid pace of job growth. One such constraint mentioned is the possibility that businesses are struggling to find available workers due to the tightening labor market. As the pool of unemployed or underemployed workers diminishes, it becomes increasingly challenging for businesses to fill job vacancies, which can hinder their ability to expand operations and meet growing demand.

When businesses face difficulties in hiring workers, it can lead to labor shortages, wage pressures, and potentially slower economic growth. Additionally, constraints on labor supply can prompt businesses to explore alternatives such as automation or outsourcing, which may have implications for employment levels and wage dynamics.

Overall, while the strong job gains reflect a healthy labor market and economic growth, the anticipation of a slowdown underscores the importance of monitoring labor market dynamics, workforce participation rates, and policies aimed at addressing labor market challenges to sustain long-term economic expansion.

Historically, economists and investors have been confident in the Fed’s ability to control inflation and maintain it around the 2% target. The focus has typically been on the strategies the Fed would employ to achieve this target rather than on doubts about its effectiveness.

However, recent developments suggest a departure from this confidence. Economists have begun revising their forecasts for inflation upward, indicating a growing acknowledgment of potential challenges in controlling inflation within the desired range. This adjustment in inflation forecasts occurred even before the release of recent data indicating higher-than-expected price levels.

The mention of “hotter-than-expected price data” suggests that inflationary pressures may be building more rapidly than previously anticipated. This unexpected surge in prices could prompt further revisions to inflation forecasts and raise questions about the Fed’s ability to rein in inflation effectively.

Overall, the passage highlights a shift in sentiment regarding inflation management, signaling increased uncertainty among economists and investors about the path ahead and the potential measures required to achieve the Fed’s inflation target.

For over two years, economists have been gradually increasing their forecasts for interest rates. This upward trend in interest rate forecasts has been driven by two main factors:

Despite concerns about slowing growth, the economy has demonstrated resilience, showing few signs of a significant slowdown. Strong economic growth typically leads to higher inflationary pressures, prompting expectations of tighter monetary policy by the Federal Reserve to prevent the economy from overheating.

Inflation has remained above the Fed’s 2% target for an extended period. Persistent inflationary pressures have raised concerns among economists about the potential for inflation to become entrenched, necessitating more aggressive monetary policy action by the Fed to bring it back to target levels.

However, there was a notable exception in January, where economists forecasted steeper rate cuts than in previous months. This deviation from the upward trend in interest rate forecasts occurred because economists were confident that inflation was nearing its target and that the Fed’s efforts to control inflation were succeeding.

Now, economists have reverted to expecting a higher path for interest rates. This shift suggests a renewed focus on the potential risks of inflation and the need for the Fed to tighten monetary policy to ensure price stability. It also reflects a reassessment of economic conditions and the outlook for growth, inflation, and interest rates in light of recent developments.

In the ebb and flow of the global economy, job layoffs are often a harsh reality. Despite efforts to maintain stability, companies occasionally face circumstances that necessitate workforce reductions. The year 2024 has been no exception, with several prominent organizations undergoing restructuring that led to employee terminations. These events serve as poignant reminders of the volatile nature of modern business landscapes and offer valuable lessons for both employers and employees alike. Navigating the Waves of Job Layoffs: Lessons from Companies in 2024

In early 2024, Tesla, the innovative electric vehicle manufacturer, announced a significant workforce reduction. The decision came as part of the company’s strategic shift towards enhancing operational efficiency and focusing on core business priorities. While Tesla cited reasons such as streamlining processes and adapting to market dynamics, the move nonetheless impacted a notable portion of its workforce. This underscores the importance of agility in responding to industry changes, albeit with sensitivity towards affected employees.

Another notable instance occurred in the hospitality sector, with Airbnb announcing layoffs in response to evolving market conditions. The company, known for its disruptive approach to accommodation services, faced headwinds amid shifting consumer preferences and regulatory pressures. Consequently, Airbnb made the difficult decision to downsize certain divisions, aligning its resources with strategic objectives. This highlights the imperative for businesses to anticipate and adapt to market disruptions proactively.

In a bid to streamline operations and foster innovation, IBM embarked on a restructuring initiative in 2024. The technology giant aimed to realign its workforce to focus on emerging technologies such as artificial intelligence and cloud computing. While these efforts signaled IBM’s commitment to remaining competitive in a rapidly evolving tech landscape, they also resulted in workforce reductions. The case of IBM underscores the importance of balancing short-term adjustments with long-term strategic vision.

Even stalwarts of the retail industry were not immune to the winds of change. In 2024, Walmart, the world’s largest retailer, announced layoffs affecting certain corporate positions. The decision came amidst a broader transformation aimed at enhancing operational efficiency and accelerating digital initiatives. Despite its formidable market presence, Walmart recognized the need to adapt to shifting consumer behaviors and technological advancements, albeit with implications for its workforce.

Key Takeaways for Businesses and Employees

The aforementioned instances of job layoffs in 2024 offer valuable insights for businesses and employees navigating turbulent waters:

1. Adaptability is Paramount: Companies must remain agile in responding to market dynamics, embracing change as an opportunity for growth rather than solely a challenge to be endured.

2. Strategic Vision Guides Decision-making: While short-term adjustments may be necessary, organizations must align workforce decisions with long-term strategic objectives to ensure sustained relevance and competitiveness.

3. Prioritize Employee Support: Amidst restructuring efforts, companies should prioritize supporting affected employees through comprehensive transition assistance programs, including retraining and outplacement services.

4. Resilience and Upskilling: Employees, on their part, should cultivate resilience and invest in upskilling to remain adaptable in dynamic job markets, enhancing their employability and future prospects.

In conclusion, job layoffs in 2024 serve as poignant reminders of the inherent volatility of modern business environments. By embracing adaptability, maintaining strategic foresight, and prioritizing employee support, companies can navigate these challenges while fostering resilience and sustainable growth. Similarly, employees can seize opportunities for self-improvement and skill development, empowering themselves to thrive amidst change. Ultimately, in the ever-changing landscape of work, the ability to weather storms and emerge stronger lies in our collective capacity to evolve and innovate.