Recent news reports highlight key concerns and sentiments expressed by Federal Reserve policymakers during a recent meeting. Fed Expresses Uncertainty About Inflation

Sticky Price Pressures: The persistence of inflation in certain sectors, where prices do not adjust downward easily even when economic conditions change. These sectors might include housing, healthcare, and some services where costs are less flexible.

Uncertainty: The policymakers’ uncertainty about these sticky price pressures indicates that they are facing challenges in predicting and managing inflation dynamics. This uncertainty can stem from various factors, such as supply chain disruptions, labor market tightness, or geopolitical events affecting commodity prices. Fed Expresses Uncertainty About Inflation

Fed Expresses Uncertainty About Inflation

Lack of Confidence in Achieving the 2% Inflation Goal:

Recent Data: The reference to recent data suggests that the economic indicators available at the time of the meeting were not sufficiently reassuring. These indicators likely include measures of consumer prices, producer prices, wage growth, and perhaps broader economic activity.

2% Inflation Goal: The Federal Reserve’s long-term target is to maintain inflation at around 2%, which is considered conducive to economic stability and growth. The lack of confidence in reaching this goal suggests that inflation might be running higher than desired, or that there is significant variability in inflation rates across different sectors.

Implications for Monetary Policy:

Policy Decisions: Given the uncertainty and lack of confidence, policymakers might adopt a more cautious approach. This could mean they are hesitant to either aggressively hike interest rates (which could stifle growth) or cut them (which could risk higher inflation).

Communication and Forward Guidance: The report underscores the importance of clear communication from the Fed. Policymakers need to manage expectations by conveying their concerns and the data dependency of their decisions, maintaining credibility and stability in financial markets.

Economic Context:

In summary, the minutes reveal a cautious and data-driven approach by the Federal Reserve, grappling with persistent inflationary pressures and the challenge of guiding the economy towards stable and sustainable growth. The policymakers’ uncertainty and lack of confidence in meeting the 2% inflation target underscore the complexities of the current economic environment and the delicate balance required in monetary policy decisions.

Inflation, the persistent increase in the general price level of goods and services over time, can have far-reaching consequences on economies and societies. While its effects are often discussed in macroeconomic terms, the impact on small businesses, the backbone of many economies, is profound and often overlooked. This article delves into the pernicious effects of inflation specifically on small businesses, exploring how rising prices can disrupt operations, strain finances, and hamper growth prospects. The Pernicious Impact of Inflation on Small Businesses

The Pernicious Impact of Inflation on Small Business

Reduced Purchasing Power: One of the most immediate consequences of inflation for small businesses is the erosion of purchasing power. As prices rise across the board, the same amount of money buys fewer goods and services. For small businesses operating on tight budgets, this means they can afford fewer supplies, equipment, and other essentials, ultimately hindering their ability to operate efficiently and compete effectively in the market.

Increased Operating Costs: Inflation doesn’t just affect the prices of goods and services that small businesses purchase; it also impacts their operating costs. Essentials such as rent, utilities, and wages often rise alongside inflation, putting additional strain on already stretched budgets. Small businesses may find themselves forced to increase prices to offset these higher costs, risking losing customers in the process or absorbing the costs themselves, further squeezing profit margins.

Uncertainty and Planning Challenges: Inflation introduces uncertainty into the business environment, making it difficult for small businesses to plan for the future. Fluctuating prices make it challenging to accurately forecast expenses and revenues, leading to increased risk and reduced confidence in investment decisions. Small businesses may hesitate to expand or invest in new ventures, opting instead for cautious strategies that prioritize survival over growth.

Difficulty Accessing Credit: Inflation can also affect small businesses’ ability to access credit. Lenders may be hesitant to extend loans or lines of credit in inflationary environments due to the increased risk of default. Even if credit is available, small businesses may face higher interest rates, making borrowing more expensive and potentially unsustainable for those already struggling with rising costs and reduced profitability.

Competitive Disadvantage: Inflation can widen the gap between small businesses and larger competitors with greater resources and economies of scale. Small businesses may struggle to absorb price increases as efficiently or negotiate favorable terms with suppliers, putting them at a competitive disadvantage. Inflationary pressures can also lead to market consolidation, as larger firms with stronger financial positions capitalize on smaller competitors’ difficulties, further concentrating economic power.

The pernicious impact of inflation on small businesses cannot be overstated. From reduced purchasing power and increased operating costs to uncertainty and competitive disadvantages, inflation poses significant challenges for small businesses trying to thrive in increasingly volatile economic environments. Policymakers must consider the unique needs of small businesses when formulating inflation-fighting strategies, ensuring that measures aimed at stabilizing prices do not inadvertently exacerbate the challenges faced by those at the heart of the economy.

Few metrics hold as much sway and significance as interest rates. From impacting borrowing costs to influencing investment decisions, fluctuations in interest rates can reverberate throughout the global economy. Chief Financial Officers (CFOs) are key figures in navigating these dynamics, as their insights and strategies shape how businesses respond to changing interest rate environments. In this article, we delve into the perspectives of CFOs regarding the direction of interest rates, exploring their sentiments, predictions, and the implications for corporate decision-making.

CFOs Speak Out on Interest Rates

Understanding the Significance of Interest Rates: Interest rates serve as a fundamental mechanism for regulating economic activity. Central banks adjust interest rates to manage inflation, stimulate economic growth, or curb excessive borrowing. For businesses, interest rates directly influence the cost of capital, impacting investment decisions, capital expenditures, and overall financial health.

Insights from CFO Surveys: Numerous surveys and studies regularly gauge the sentiments of CFOs regarding interest rate trends. These surveys provide valuable insights into how finance leaders perceive the trajectory of interest rates and the potential implications for their organizations.

Optimism Amidst Uncertainty: CFO sentiment towards interest rates often reflects broader economic outlooks. During periods of economic expansion and stability, CFOs may express confidence in a gradual increase in interest rates, signaling robust growth prospects. Conversely, economic uncertainty or recessionary concerns may lead CFOs to anticipate rate cuts or prolonged low rates to stimulate economic activity.

Impact on Financing Decisions: Interest rate forecasts significantly influence corporate financing decisions. CFOs must weigh the benefits of accessing capital at lower rates against the potential risks of rising borrowing costs. For instance, in a low-interest-rate environment, companies may pursue debt financing for expansion projects or strategic acquisitions. Conversely, rising interest rates may prompt a shift towards equity financing or tighter capital expenditure controls to manage financial risk.

Hedging Strategies and Risk Management: CFOs employ various hedging strategies to mitigate the impact of interest rate fluctuations on their organizations. Interest rate swaps, options, and other derivative instruments enable companies to lock in favorable rates or protect against adverse movements. These risk management tactics are essential for safeguarding financial stability and ensuring resilience against volatile market conditions.

Global Macroeconomic Factors: Interest rate trends are influenced by a complex interplay of global macroeconomic factors, including geopolitical events, monetary policy decisions, and inflationary pressures. CFOs must closely monitor these developments and adapt their strategies accordingly to navigate evolving market dynamics and mitigate potential risks to their businesses.

In an ever-changing economic landscape, CFOs play a pivotal role in interpreting and responding to interest rate trends. By staying attuned to market signals, leveraging financial instruments, and implementing prudent risk management practices, CFOs can steer their organizations through uncertain times and capitalize on opportunities for sustainable growth and value creation. As interest rates continue to evolve, CFOs will remain vigilant, ensuring that their organizations remain agile and resilient in the face of economic uncertainty.

In recent months, fast food aficionados have been greeted with an unwelcome surprise: their favorite quick bites are becoming increasingly expensive. The once-affordable indulgence of a fast food meal is now putting a dent in wallets across the board. This phenomenon begs the question: why are fast food prices on the rise?

Fast Food Prices on the Rise

Supply Chain Woes

One of the primary culprits behind the surge in fast food prices is the ongoing disruption in supply chains. From farm to table, the journey of ingredients to your favorite fast food joint involves a complex network of suppliers, distributors, and manufacturers. However, disruptions like extreme weather events, labor shortages, and transportation challenges have thrown a wrench into this intricate system.

Consider the impact of climate change on agriculture. Unpredictable weather patterns and natural disasters can decimate crops, leading to shortages and increased prices for key ingredients like wheat, corn, and potatoes – staples in many fast food offerings. Furthermore, labor shortages exacerbated by the COVID-19 pandemic have led to increased wages for workers throughout the supply chain, which in turn drive up production costs.

Inflationary Pressures

Inflation, the general increase in prices over time, is another factor contributing to the uptick in fast food prices. As the cost of living rises, businesses are forced to adjust their prices to maintain profitability. The Federal Reserve’s efforts to stimulate the economy through low interest rates and monetary stimulus measures can inadvertently fuel inflationary pressures, further squeezing the margins of fast food establishments.

Menu Evolution

Another factor influencing fast food prices is the evolving nature of menus. In response to changing consumer preferences and societal trends, many fast food chains have expanded their offerings to include healthier, more sustainable options. While these menu additions may appeal to a broader customer base, they often come with higher price tags due to the use of premium ingredients and additional preparation requirements.

Navigating the New Normal

As consumers grapple with the reality of higher fast food prices, many are forced to reconsider their dining habits. Some may opt for less frequent visits to their favorite chains, while others may explore alternative dining options such as home-cooked meals or locally sourced eateries. Additionally, loyalty programs and promotional deals may become increasingly valuable as consumers seek ways to stretch their dining dollars further.

In conclusion, the rising cost of fast food is a multifaceted issue driven by supply chain disruptions, inflationary pressures, and evolving consumer preferences. While the days of dirt-cheap drive-thru meals may be a thing of the past, savvy consumers can still find ways to indulge in their favorite fast food treats without breaking the bank. However, it may require a bit more creativity and resourcefulness in navigating the ever-changing landscape of the fast food industry.

Betting against the dollar in favor of other currencies can have several consequences, especially in 2024 when global economic dynamics are in flux. Here are some potential consequences: The Consequences of Betting Against the Dollar.

Betting Against the Dollar

Currency Exchange Risk: Betting against the dollar means holding other currencies, exposing you to fluctuations in exchange rates. If the dollar strengthens relative to those currencies, you could incur losses when converting back to dollars.

Inflation Impact: If the dollar weakens significantly, it can lead to imported inflation as the cost of goods denominated in foreign currencies rises. This can erode purchasing power and lead to higher domestic prices for imported goods.

Interest Rate Differentials: Central banks may adjust interest rates to manage their respective currencies. If interest rates rise in the currencies you’re betting on, it could attract capital inflows and strengthen those currencies further. Conversely, if rates in those currencies fall or remain low, it might weaken them.

Trade Implications: A weaker dollar can make exports more competitive but imports more expensive, potentially impacting trade balances. Conversely, a stronger dollar might make imports cheaper but exports more expensive.

Asset Markets: A weaker dollar could boost asset prices denominated in other currencies, such as commodities or foreign stocks. Conversely, a stronger dollar might put pressure on those assets.

Global Economic Stability: Major shifts in currency valuations can have ripple effects throughout the global economy. It could affect the debt burdens of countries with significant dollar-denominated debt, impact international investments, and influence geopolitical dynamics.

Policy Responses: Central banks and governments may respond to currency movements with policy interventions, such as currency interventions or changes in monetary policy. These responses can have unpredictable effects on currency markets.

Speculative Risks: Betting against the dollar can be speculative and carries risks. Market sentiment and speculative activity can exacerbate currency movements, leading to sharp and unpredictable fluctuations.

Diversification Benefits: Holding assets in a mix of currencies can provide diversification benefits, spreading risk across different economic regions and currencies.

Long-Term Trends: It’s essential to consider long-term structural trends in the global economy, such as shifts in economic growth, demographic changes, technological advancements, and geopolitical developments, which can influence currency valuations over time.

Overall, betting against the dollar in favor of other currencies can offer opportunities for profit, but it’s essential to carefully assess the risks and potential consequences, especially in a dynamic and uncertain economic environment like 2024.

In an intriguing economic paradox, consumers across various sectors have been vocal about their dissatisfaction with rising prices, yet their spending habits continue to show resilience. This puzzling phenomenon raises questions about the true impact of price increases on consumer behavior and the underlying factors driving their purchasing decisions. Consumers Complain about Prices Despite Continued Spending.

The Consumer Conundrum

Amidst a backdrop of inflationary pressures and cost-of-living concerns, consumers have been increasingly vocal about the rising prices of goods and services. Social media platforms, consumer forums, and customer reviews are rife with complaints about the escalating costs of everyday necessities, ranging from groceries and fuel to housing and healthcare. These grievances often echo sentiments of frustration, anxiety, and a sense of financial strain.

However, despite these expressions of discontent, empirical data reveal a contradictory trend: consumers are not significantly scaling back their spending. Retail sales figures, e-commerce transactions, and leisure activities continue to show robust levels of consumption, suggesting that the perceived impact of price hikes on actual purchasing behavior may not be as pronounced as anticipated.

Several factors contribute to this apparent paradox. Firstly, consumers exhibit varying degrees of price sensitivity depending on the nature of the goods or services in question. While some items are considered essential and non-negotiable, others are more discretionary, allowing consumers greater flexibility in adjusting their spending patterns. This segmentation in consumer preferences underscores the nuanced relationship between price perception and purchasing decisions.

Moreover, psychological biases and cognitive heuristics play a pivotal role in shaping consumer behavior. The phenomenon of “anchoring,” whereby individuals use initial price references as benchmarks for subsequent evaluations, can mitigate the perceived severity of price increases. Additionally, the concept of “mental accounting” leads consumers to compartmentalize their budgets, allowing them to justify expenditure in certain categories despite overall budgetary constraints.

Furthermore, the influence of external factors, such as income levels, employment stability, and access to credit, cannot be overlooked. In times of economic uncertainty, consumers may prioritize maintaining their standard of living or hedging against future uncertainties, thereby exhibiting a higher tolerance for price fluctuations.

From a broader economic perspective, the disconnect between consumer complaints and spending behavior underscores the complex interplay between micro-level perceptions and macro-level indicators. While individual grievances may reflect genuine concerns about affordability and purchasing power, aggregate spending data paint a more nuanced picture of consumer sentiment and resilience in the face of economic challenges.

Addressing this paradox requires a multifaceted approach that considers both the structural factors driving price inflation and the psychological mechanisms shaping consumer decision-making. Policymakers, businesses, and financial institutions must adopt strategies that address the root causes of inflation while also fostering consumer confidence and affordability.

In conclusion, the phenomenon of consumers complaining about prices while continuing to spend highlights the intricate dynamics of modern consumption patterns. By understanding the underlying drivers and motivations behind this paradox, stakeholders can develop more effective strategies to navigate evolving economic landscapes and meet the diverse needs of consumers in an increasingly complex market environment.

As streaming services like Netflix continue to dominate the entertainment landscape, recent efforts to curb password sharing have sparked a debate about the future of digital content consumption. Netflix’s decision to crack down on password sharing has raised questions about fairness, convenience, and the evolving nature of subscription-based models. The Impact of the Netflix Password Crackdown.

Netflix Password Crackdown –

The move comes as streaming platforms grapple with the challenge of retaining paying subscribers while also combating unauthorized account sharing. By enforcing stricter measures to ensure that only authorized users have access to their accounts, Netflix aims to protect its revenue stream and uphold agreements with content creators.

However, this crackdown has prompted mixed reactions from consumers and industry experts alike. While some applaud Netflix’s efforts to protect its business interests and maintain a level playing field, others argue that it may alienate loyal customers and hinder organic growth.The Impact of the Netflix Password Crackdown

One of the key concerns revolves around the impact on user experience. For many households, sharing a Netflix account has become a common practice, allowing family members and friends to enjoy content without the burden of additional expenses. By restricting password sharing, Netflix risks disrupting this convenience and potentially driving users to seek alternative, more affordable options.

Moreover, critics argue that the crackdown may disproportionately affect lower-income households, who rely on shared accounts as a cost-saving measure. In an era marked by economic uncertainty, access to affordable entertainment options has become increasingly important for many individuals and families.

On the other hand, proponents of the crackdown argue that it is a necessary step to protect the integrity of subscription-based services. By deterring unauthorized account sharing, streaming platforms can ensure that content creators receive fair compensation for their work. This, in turn, could incentivize the production of high-quality content and foster a more sustainable entertainment ecosystem.

Additionally, stricter enforcement of user authentication measures could help streaming services gather more accurate data on viewer preferences and behavior. This valuable insight can inform content curation efforts, leading to a more personalized and engaging viewing experience for subscribers.

The company added 9.33 million subscribers in the first quarter, more than five times the number of customers it added during the same period a year earlier, with its efforts to limit password sharing continuing to bear fruit. Netflix began limiting password sharing in earnest about a year ago.

Netflix ended the first quarter with 269.6 million paying customers globally and said it now has an audience of more than a half billion people.

While some entertainment companies struggle with password-sharing crackdowns and Netflix is already benefiting.

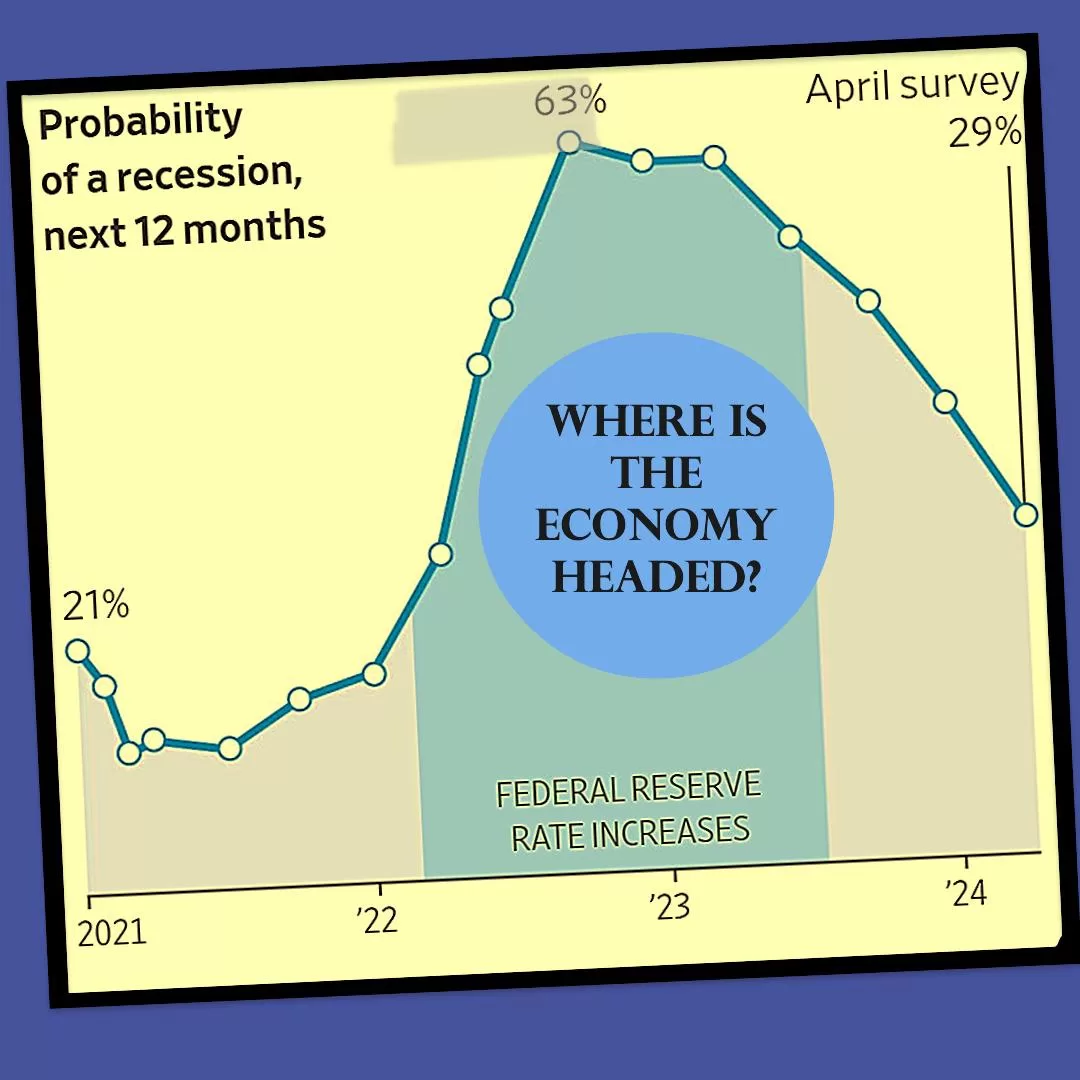

Immigration can contribute to economic growth by expanding the labor force, increasing productivity, and driving innovation. Immigrants often fill essential roles in industries experiencing labor shortages, helping to sustain and grow businesses. Where is the Economy Headed in 2024?

Where is the Economy Headed in 2024?

Consumer spending is a critical driver of economic growth, as it accounts for a significant portion of overall economic activity. When consumers feel confident about their financial situation and job prospects, they are more likely to spend on discretionary items, leading to increased demand and economic expansion. Where is the Economy Headed in 2024?

Given the robust growth fueled by these factors, economists are optimistic about the economy’s near-term outlook. Confidence in job security is likely bolstering consumer sentiment, encouraging continued spending and economic momentum. As a result, economists don’t foresee the economy entering a recession in the coming year.

It’s important to monitor various economic indicators and external factors to assess the sustainability of this growth trajectory and identify any potential risks or challenges that may arise in the future.

The job gains surpassing forecasts indicate a robust labor market, potentially buoyed by factors such as increased immigration contributing to population growth. A growing population can create additional demand for goods and services, which in turn stimulates job creation across various sectors of the economy.

However, economists’ anticipation of an imminent slowdown suggests that there are constraints on the labor market’s ability to sustain this rapid pace of job growth. One such constraint mentioned is the possibility that businesses are struggling to find available workers due to the tightening labor market. As the pool of unemployed or underemployed workers diminishes, it becomes increasingly challenging for businesses to fill job vacancies, which can hinder their ability to expand operations and meet growing demand.

When businesses face difficulties in hiring workers, it can lead to labor shortages, wage pressures, and potentially slower economic growth. Additionally, constraints on labor supply can prompt businesses to explore alternatives such as automation or outsourcing, which may have implications for employment levels and wage dynamics.

Overall, while the strong job gains reflect a healthy labor market and economic growth, the anticipation of a slowdown underscores the importance of monitoring labor market dynamics, workforce participation rates, and policies aimed at addressing labor market challenges to sustain long-term economic expansion.

Historically, economists and investors have been confident in the Fed’s ability to control inflation and maintain it around the 2% target. The focus has typically been on the strategies the Fed would employ to achieve this target rather than on doubts about its effectiveness.

However, recent developments suggest a departure from this confidence. Economists have begun revising their forecasts for inflation upward, indicating a growing acknowledgment of potential challenges in controlling inflation within the desired range. This adjustment in inflation forecasts occurred even before the release of recent data indicating higher-than-expected price levels.

The mention of “hotter-than-expected price data” suggests that inflationary pressures may be building more rapidly than previously anticipated. This unexpected surge in prices could prompt further revisions to inflation forecasts and raise questions about the Fed’s ability to rein in inflation effectively.

Overall, the passage highlights a shift in sentiment regarding inflation management, signaling increased uncertainty among economists and investors about the path ahead and the potential measures required to achieve the Fed’s inflation target.

For over two years, economists have been gradually increasing their forecasts for interest rates. This upward trend in interest rate forecasts has been driven by two main factors:

Despite concerns about slowing growth, the economy has demonstrated resilience, showing few signs of a significant slowdown. Strong economic growth typically leads to higher inflationary pressures, prompting expectations of tighter monetary policy by the Federal Reserve to prevent the economy from overheating.

Inflation has remained above the Fed’s 2% target for an extended period. Persistent inflationary pressures have raised concerns among economists about the potential for inflation to become entrenched, necessitating more aggressive monetary policy action by the Fed to bring it back to target levels.

However, there was a notable exception in January, where economists forecasted steeper rate cuts than in previous months. This deviation from the upward trend in interest rate forecasts occurred because economists were confident that inflation was nearing its target and that the Fed’s efforts to control inflation were succeeding.

Now, economists have reverted to expecting a higher path for interest rates. This shift suggests a renewed focus on the potential risks of inflation and the need for the Fed to tighten monetary policy to ensure price stability. It also reflects a reassessment of economic conditions and the outlook for growth, inflation, and interest rates in light of recent developments.

Federal Reserve Chairman Tempers Expectations of Rate Cuts

Federal Reserve Chairman Jerome Powell’s recent remarks have tempered expectations of imminent rate cuts, signaling a cautious approach to monetary policy amidst evolving economic conditions. In this article, we examine Powell’s statements, analyze their implications for interest rates and financial markets, and explore the factors shaping the Federal Reserve’s policy stance in the current economic landscape.

Jerome Powell Tempers Expectations of Rate Cuts

Powell’s Comments:

During a recent press conference, Jerome Powell acknowledged the challenges facing the US economy but expressed confidence in its underlying strength and resilience. While acknowledging inflationary pressures and downside risks, Powell emphasized the Federal Reserve’s commitment to maintaining a balanced approach to monetary policy, anchored by its dual mandate of price stability and maximum employment. Powell’s comments underscored the Federal Reserve’s stance of patience and data-dependence in navigating the uncertainties of the post-pandemic recovery. Federal Reserve Chairman Tempers Expectations of Rate Cuts.

Market Reaction:

Powell’s tempered expectations of rate cuts were met with a mixed reaction from financial markets. Equity markets initially reacted positively to Powell’s reassurance of the Federal Reserve’s commitment to supporting economic growth, with stock prices edging higher. However, bond markets exhibited more volatility, reflecting uncertainty about the trajectory of interest rates and inflation expectations. Overall, Powell’s remarks underscored the delicate balancing act facing policymakers as they seek to calibrate monetary policy in response to evolving economic data and market dynamics.

Economic Considerations:

Powell’s cautious tone reflects the Federal Reserve’s assessment of the current economic landscape, which is characterized by a complex interplay of factors. While the US economy has made significant strides in recovering from the pandemic-induced downturn, lingering challenges remain, including supply chain disruptions, labor market dynamics, and inflationary pressures. The Federal Reserve’s decision-making process is informed by a wide range of economic indicators, including employment data, inflation metrics, consumer spending, and business investment, which collectively shape its policy outlook. Federal Reserve Chairman Tempers Expectations of Rate Cuts.

Policy Outlook:

Looking ahead, Powell’s remarks suggest that the Federal Reserve is unlikely to pursue aggressive rate cuts in the near term. Instead, policymakers are likely to maintain their accommodative stance, keeping interest rates low and continuing asset purchases to provide support to the economy. However, the Federal Reserve remains vigilant about inflationary pressures and will adjust its policy stance as warranted by evolving economic conditions. Powell’s comments underscore the importance of flexibility and adaptability in navigating the uncertainties of the recovery and ensuring the Federal Reserve’s ability to fulfill its dual mandate effectively.

Conclusion:

Jerome Powell’s tempered expectations of rate cuts reflect the Federal Reserve’s cautious approach to monetary policy in the current economic environment. As policymakers navigate the complexities of the post-pandemic recovery, they remain committed to supporting economic growth while ensuring price stability and maximum employment. Powell’s remarks highlight the importance of clear communication, data-driven decision-making, and a nimble policy framework in guiding the Federal Reserve’s response to evolving economic conditions and market dynamics.

China’s persistent problem of overcapacity in various industries is proving to be a double-edged sword, with far-reaching consequences for both domestic and global markets. In this article, we delve into the reasons behind China’s overcapacity, analyze its impact on industries and economies, and explore the challenges and repercussions it presents for policymakers, businesses, and stakeholders.

Understanding China’s Overcapacity:

China’s overcapacity stems from years of rapid industrial expansion fueled by government-led investment, subsidies, and incentives. In its drive for economic growth and global competitiveness, China has heavily invested in sectors such as steel, aluminum, cement, and solar panels, leading to a glut of production capacity that far exceeds domestic and global demand.

Challenges in Managing Overcapacity:

China’s overcapacity poses numerous challenges for policymakers and industry leaders. Excess production capacity undermines market efficiency, distorts pricing mechanisms, and exacerbates competition, leading to downward pressure on prices, profitability, and investment returns. Moreover, overcapacity fuels concerns about environmental degradation, resource depletion, and energy consumption, as industries struggle to absorb excess output and manage waste.

The Consequences of China’s Overcapacity

Impact on Global Markets:

The repercussions of China’s overcapacity extend beyond its borders, affecting global markets and trade dynamics. Excess Chinese production floods international markets, driving down prices and undercutting producers in other countries. This phenomenon, often referred to as “dumping,” has sparked trade disputes, anti-dumping measures, and retaliatory actions by trading partners seeking to protect their domestic industries and market share.

Strain on State-Owned Enterprises:

China’s state-owned enterprises (SOEs) bear the brunt of overcapacity, grappling with financial losses, debt burdens, and inefficiencies resulting from excess production. SOEs, often supported by government subsidies and preferential policies, face pressure to maintain employment, social stability, and political legitimacy, even as they grapple with overcapacity and market challenges. Balancing economic imperatives with social and political objectives poses a daunting task for Chinese policymakers and SOE managers.

Shift Towards Quality and Innovation:

In response to the challenges posed by overcapacity, China is increasingly emphasizing quality, innovation, and efficiency as drivers of economic growth and competitiveness. The government has rolled out initiatives to upgrade industries, promote technological innovation, and foster a transition towards higher value-added production. By shifting focus from quantity to quality, China aims to address overcapacity while fostering sustainable, innovation-driven growth.

Conclusion:

China’s overcapacity presents a complex and multifaceted challenge with profound implications for domestic and global economies. As China grapples with excess production capacity, policymakers, businesses, and stakeholders must collaborate to find sustainable solutions that balance economic imperatives with environmental, social, and geopolitical considerations. By addressing the root causes of overcapacity, fostering innovation, and promoting market-oriented reforms, China can mitigate the negative impacts of excess capacity while charting a path towards sustainable and inclusive economic development.