Our accounts receivable factoring program can be the ideal source of financing for businesses which are growing and need cash quickly.

Program Overview $100,000 to $30 Million Non-Recourse No Audits No Financial Covenants No Long-Term Commitment Most businesses with strong customers are eligible

We like challenging deals : Start-ups Turnarounds Historic Losses Customer Concentrations Poor Personal Credit Character Issues

We focus on the quality of your client’s accounts receivable, ignoring their financial condition.

April 15th is the tax filing deadline in the United States mostly because of historical, administrative, and practical reasons:

1. Historical Timeline

When the federal income tax was first introduced with the 16th Amendment in 1913, the original filing deadline was March 1st.

In 1918, it moved to March 15th to give the IRS more time.

Then in 1955, it was pushed to April 15th, where it remains today.

2. Why April 15th Specifically?

The IRS chose April 15th for a few practical reasons:

It spreads out the workload for the IRS and tax professionals.

It gives people more time after the end of the calendar year (December 31st) to gather documents, receive W-2s and 1099s, and prepare.

It avoids the early part of the year when people are still catching up from the holidays.

It gives the government a little extra time to hold onto any tax payments before issuing refunds.

3. Adjustments for Weekends or Holidays

If April 15th falls on a weekend or a holiday (like Emancipation Day in D.C., which is on April 16), the deadline shifts to the next business day.

The federal income tax exists mainly to fund the operations of the federal government. But the story behind it is pretty fascinating, and it wasn’t always a thing.

🌱 The Origin of Federal Income Tax

Before income tax, the U.S. government got most of its money from tariffs (taxes on imported goods), excise taxes, and land sales.

But as the country grew — especially with wars and industrialization — those sources just weren’t enough.

💣 Civil War: The First Income Tax (1861)

The first federal income tax was a temporary measure to fund the Union Army during the Civil War.

It was repealed after the war ended.

🧑⚖️ The Supreme Court Gets Involved (1895)

Congress tried to bring back the income tax with the Wilson-Gorman Tariff Act of 1894, but the Supreme Court struck it down in Pollock v. Farmers’ Loan & Trust Co., saying it was unconstitutional — because it was a direct tax not apportioned by population, which the Constitution originally forbade.

🧾 Enter the 16th Amendment (1913)

To solve that issue, the 16th Amendment was ratified: “The Congress shall have power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States…”

This legally enabled the federal government to tax personal and corporate income, regardless of population or state.

💰 Why It Matters

The income tax allows the government to:

Fund public services like roads, education, defense, and social programs (Social Security, Medicare, etc.).

Respond to economic crises and national emergencies (like wars, natural disasters, pandemics).

Redistribute wealth through progressive taxation, where higher earners pay a higher percentage.

📈 Growth Over Time

What started as a tiny tax on the wealthiest Americans has grown into the main source of revenue for the federal government.

Today, individual income taxes make up around half of all federal revenue.

Alright, let’s follow the money! Here’s a simplified breakdown of where your federal income tax dollars go — based on recent federal budget data:

🧾 Where Your Tax Dollars Go (Rounded Averages)

1. 🧓 Social Security — ~22%

This funds retirement benefits, disability insurance, and survivors’ benefits.

It’s kind of like paying forward into a big national retirement system.

2. 🏥 Medicare, Medicaid, and Other Health Programs — ~25%

Medicare helps cover healthcare for people 65+.

Medicaid supports low-income families and individuals.

Other health programs include things like CHIP (Children’s Health Insurance Program) and public health funding.

3. 💣 Defense and Military — ~13–15%

Covers salaries, equipment, R&D, weapons systems, military aid to allies, and operations (like bases around the world).

4. 🏦 Interest on National Debt — ~10%

The U.S. borrows money constantly, and just like credit card debt, we have to pay interest.

This is basically the cost of maintaining the national debt (which is in the trillions).

5. 👨👩👧👦 Social Safety Net Programs — ~10%

Includes food assistance (like SNAP), unemployment benefits, housing aid, child tax credits, etc.

Designed to support low-income and vulnerable citizens.

6. 📚 Education, Infrastructure, Science, and More — ~8%

Funding for federal education programs, transportation (roads, bridges, trains), clean energy, space exploration, and scientific research.

7. 🏛️ Government Operations — ~7%

Running federal departments, agencies, courts, Congress, the White House, etc.

🔍 Example: For Every $100 You Pay in Income Tax…

Program/Area

Approx. Amount

Medicare & Health

$25

Social Security

$22

Military & Defense

$15

Interest on Debt

$10

Safety Net Programs

$10

Infrastructure & Science

$8

Government Ops

$7

Other (Foreign aid, environment, etc.)

$3

🧠 Cool Fact:

Foreign aid is only about 1% of the federal budget — way less than most people think.

The book argues that Artificial Intelligence (AI) is fundamentally transforming how businesses operate and compete, leading to the emergence of new digital giants and requiring traditional firms to rethink their strategies, operating models, and leadership. It emphasizes the shift towards AI-centric organizations powered by data, algorithms, and networks, and explores the strategic collisions between digital and traditional firms, along with the ethical and societal implications of this transformation.

Key Ideas and Facts:

1. The Transformative Power of AI and the Rise of Digital Firms:

Artificial Intelligence is reshaping competitive landscapes and impacting businesses across all sectors. The book introduces the “Age of AI” as a period of profound transformation.

Digital companies differ significantly from conventional firms, leveraging AI to create entirely new business models.

These firms build value through “digital operating models” that are inherently scalable, multisided, and capable of continuous improvement.

Examples like Ant Financial (Alipay), Amazon, Netflix, Ocado, and Peloton illustrate how digitizing operating processes with algorithms and networks leads to transformative market impact.

Ant Financial’s MYbank utilizes vast amounts of data and AI algorithms to assess creditworthiness and offer small loans efficiently: “Ant uses that data to compare good borrowers (those who repay on time) with bad ones (those who do not) to isolate traits common in both groups. Those traits are then used to calculate credit scores. All lending institutions do this in some fashion, of course, but at Ant the analysis is done automatically on all borrowers and on all their behavioral data in real time.”

Netflix leverages streaming data to personalize user experience and predict customer loyalty: “We receive several million stream plays each day, which include context such as duration, time of day and device type.”

2. Rethinking the Firm: Business and Operating Models in the Digital Age:

The book differentiates between a firm’s business model (how it creates and captures value) and its operating model (how it delivers that value).

Digital firms excel at business model innovation, often separating value creation and capture and leveraging diverse stakeholders.

“A company’s business model is therefore defined by how it creates and captures value from its customers.”

The operating model is the “actual enabler of firm value and its ultimate constraint.” Digital operating models are characterized by software, networks, and AI.

Digitization leads to processes that are “infinitely scalable” and “intrinsically multisided,” allowing firms to expand their scope and create multiplicative value.

3. The Artificial IntelligenceFactory: Data, Algorithms, and Continuous Improvement:

Advanced digital firms operate like an “AI Factory,” with a core system of data, decision algorithms, and machine learning driving continuous improvement and innovation.

Data is the foundation, requiring industrialized gathering, preparation, and governance.

Algorithms are the tools that use data to make decisions and predictions. Various types of algorithms (supervised, unsupervised, reinforcement learning) are employed.

Experimentation platforms are crucial for testing and refining algorithms and service offerings.

“After the data is gathered and prepared, the tool that makes the data useful is the algorithm—the set of rules a machine follows to use data to make a decision, generate a prediction, or solve a particular problem.”

4. Rearchitecting the Firm: Transitioning to an AI-Powered Organization:

Traditional firms need to “rearchitect” their operations and architecture to integrate AI capabilities and achieve agility.

This involves moving away from siloed, functionally organized structures towards more modular and interconnected systems.

The historical evolution of operating models, from craft production to mass production, provides context for the current digital transformation.

Breaking down “organizational silos” and embracing modular design are key to enabling AI integration.

5. Becoming an AI Company: Key Steps for Transformation:

The book outlines steps for traditional businesses to transform into Artificial Intelligence -powered organizations, focusing on building foundational capabilities in data, algorithms, and infrastructure.

This often involves overcoming resistance to change and fostering a new mindset across the organization.

Examples like Microsoft’s internal transformation highlight the challenges and opportunities in this process.

6. Strategy for a New Age: Navigating the Digital Landscape:

Strategic frameworks and tools need to adapt to the digitally-driven, AI-powered world.

Network effects (where the value of a product or service increases with the number of users) are a critical competitive advantage for digital firms.

“Generally speaking, the more network connections, the greater the value; that’s the basic mechanism generating the network effect.”

Understanding the dynamics of network value creation and capture, including factors like multihoming and network bridging, is essential for strategic decision-making.

Analyzing the potential of a firm’s strategic networks and identifying opportunities for synergy and expansion is crucial.

7. Strategic Collisions: Competition Between Digital and Traditional Firms:

The book explores the competitive dynamics between AI-driven/digital and traditional/analog firms, leading to market disruptions.

Digital entrants can often outperform incumbents by leveraging AI for superior efficiency, personalization, and scale.

The example of a financial services entrant using AI for creditworthiness demonstrates this: “Consider a financial services entrant that uses AI to evaluate creditworthiness by analyzing hundreds of variables, outperforming legacy methods. This approach enables the company to approve significantly more borrowers while automating most loan processes.”

Established businesses face a “blank-sheet opportunity” to reimagine their operating models with AI agents, potentially diminishing the competitive advantage of scale held by larger incumbents.

8. The Ethics of Digital Scale, Scope, and Learning:

The ethical implications of AI scaling, data use, and its impact on society are examined.

This includes concerns about algorithmic bias, privacy erosion, the spread of misinformation, and the potential for increased inequality.

The book acknowledges that “Human bias Is a Huge Problem for AI.”

The need for new responsibilities and frameworks to address these ethical challenges is highlighted.

9. The New Meta: Transforming Industries and Ecosystems:

AI is transforming industries and ecosystems, creating “mega digital networks” with “hub firms” that control essential connections.

These hub firms, like Amazon and Tencent, exert significant influence and face increasing scrutiny from regulators.

The boundaries between industries are blurring as AI enables firms to recombine capabilities and offer novel services.

10. A Leadership Mandate: Skills and Mindsets for the AI Era:

The book concludes by exploring the key leadership challenges, skills, and mindsets needed to exploit the strategic opportunity and thrive in the AI era.

Leaders must foster a culture of experimentation, embrace data-driven decision-making, and navigate the ethical complexities of Artificial Intelligence.

The importance of collective wisdom, community engagement, and a sense of responsibility for the broader societal impact of Artificial Intelligenceis emphasized.

Quotes Highlighting Key Themes:

“Artificial intelligence is transforming the way firms function and is restructuring the economy.” (Chapter 1 Summary)

“Strategy, without a consistent operating model, is where the rubber meets the air.” (Chapter on Operating Models)

“The core of the new firm is a scalable decision factory, powered by software, data, and algorithms.” (Chapter 3 Summary)

“The value of a firm is shaped by two concepts. The first is the firm’s business model, defined as the way the firm promises to create and capture value. The second is the firm’s operating model, defined as the way the firm delivers the value to its customers.” (Chapter on Business Models)

Overall Significance:

“Competing in the Age of AI” provides a comprehensive framework for understanding the profound impact of Artificial Intelligenceon business and competition. It offers valuable insights for both traditional organizations seeking to adapt and new digital ventures aiming to disrupt markets. The book stresses the critical interplay between technology, strategy, operations, and ethics in navigating the evolving digital landscape and emphasizes the imperative for forward-thinking leadership in the age of AI

According to Competing in the Age of AI, what is the transformative impact of AI on businesses, and how is it changing competitive landscapes? Provide two specific examples mentioned in the book summary.

How do digital companies, enabled by AI, fundamentally differ in their business models compared to conventional firms? Explain one way AI facilitates these new business models.

Describe the “AI Factory” concept. What are the key components that drive continuous improvement and innovation in advanced digital firms?

Why is it crucial for companies to rearchitect their operations to integrate AI capabilities? Mention one specific benefit of this rearchitecting process.

Outline two key steps a traditional business should undertake to transform into an AI-powered organization.

What are “strategic collisions” as described in the book? Explain the nature of the competition between AI-driven and traditional firms.

Discuss one significant ethical implication arising from the scaling of AI, the use of large datasets, or the societal impact of AI technologies.

How is AI transforming industries and ecosystems, leading to the emergence of a “new meta”? Briefly explain the role of “hub firms” in this context.

What are the two primary components that define a firm’s value, according to the excerpts? Briefly describe each component.

Explain the concept of “network effects” and provide a concise example of how it amplifies value for users in a digital platform.

Quiz Answer Key

AI is transforming businesses by fundamentally altering how they function and compete, leading to reshaped competitive landscapes. Examples include a financial services entrant using AI for superior creditworthiness evaluation and established businesses using AI agents to reimagine operating models.

Digital companies with AI have business models where value creation and capture can be separated and often involve different stakeholders, unlike the typically direct customer-based model of conventional firms. AI enables this by facilitating new ways to collect and leverage data for value creation (e.g., free services subsidized by advertisers).

The “Artificial Intelligence Factory” is a system used by advanced digital firms comprising data, decision algorithms, and machine learning. This system continuously analyzes data, refines algorithms, and improves decision-making processes, driving ongoing innovation.

Companies need to restructure their operations to integrate AI capabilities to enhance agility, improve efficiency, and leverage the power of data-driven insights for better decision-making. One benefit is the ability to automate processes and augment human intelligence.

Two key steps include developing an AI strategy aligned with business goals and building the necessary data infrastructure and talent to support AI-driven processes and tools.

“Strategic collisions” refer to the competitive clashes between established traditional (“analog”) firms and emerging AI-driven (“digital”) firms. These collisions often result in market disruptions as digital firms leverage AI for new efficiencies and business models.

One significant ethical implication is algorithmic bias, where AI systems trained on biased data can perpetuate or even amplify societal inequalities in areas like lending, hiring, or even criminal justice.

The “new meta” describes how AI fosters the creation of mega digital networks and transforms industries by connecting previously disparate sectors. “Hub firms” are central players in these networks, controlling key connections and shaping competitive dynamics across multiple industries.

The two primary components are the firm’s business model, which is how the firm promises to create and capture value, and the firm’s operating model, which is how the firm delivers that promised value to its customers.

Network effects occur when the value of a product or service increases for each user as more users join the network. For example, the value of a social media platform increases for each user as more of their friends and contacts join and become active.

Essay Format Questions

Analyze the key differences between the operating models of traditional firms and AI-native digital firms as described in Competing in the Age of AI. Discuss how these differences impact their ability to innovate and compete in the current economic landscape.

Evaluate the concept of the “AI Factory” as presented by Iansiti and Lakhani. Discuss the critical elements necessary for a company to successfully implement and leverage such a system for sustained competitive advantage.

Discuss the strategic implications of “strategic collisions” for both traditional and AI-driven businesses. What strategies can each type of firm employ to navigate and potentially thrive amidst these disruptive competitive dynamics?

Explore the ethical challenges posed by the increasing prevalence of AI in business and society, as highlighted in Competing in the Age of AI. What responsibilities do business leaders and policymakers have in addressing these challenges?

Based on the insights from Competing in the Age of AI, outline the key leadership skills and mindsets required for executives to successfully guide their organizations through the ongoing transformation driven by artificial intelligence.

Glossary of Key Terms

AI Factory: A system of data, decision algorithms, and machine learning used by advanced digital firms to drive continuous improvement and innovation through data-driven insights and automated processes.

Business Model: The way a firm promises to create and capture value for its customers, encompassing its value proposition and revenue generation mechanisms.

Operating Model: The way a firm delivers the value promised in its business model to its customers, encompassing its organizational structure, processes, and technologies.

Strategic Collisions: The competitive dynamics and market disruptions that occur when AI-driven digital firms with new business and operating models compete against traditional analog firms.

Network Effects: The phenomenon where the value of a product or service increases for each user as more users join the network, creating positive feedback loops and potential for rapid growth.

Digital Amplification: The ways in which digital technologies, particularly AI, can magnify the scale, scope, and learning capabilities of firms, leading to significant market impact.

Rearchitecting the Firm: The process of restructuring a company’s operations and technological infrastructure to effectively integrate Artificial Intelligence capabilities and achieve greater agility.

Hub Firms: Companies that become central orchestrators in digital ecosystems, controlling key connections and data flows across multiple industries.

Multihoming: The practice of users or participants engaging with multiple competing platforms within the same market (e.g., a driver working for both Uber and Lyft).

Disintermediation: The removal of intermediaries or middlemen from a value chain, often facilitated by digital platforms and AI, leading to more direct interactions between producers and consumers.

For small manufacturers, navigating the global economy means walking a tightrope between fluctuating material costs, tight production schedules, and often thin profit margins. When a trade war strikes—bringing new tariffs, disrupted supply chains, and payment delays—it can push even well-run businesses into a cash crunch.

That’s where accounts receivable factoring comes in. It offers an immediate and flexible source of working capital, giving small manufacturers the breathing room they need to keep production running.

What Is Accounts Receivable Factoring? Factoring is a financing method where a business sells its unpaid invoices to a factoring company at a discount. The business receives up to 90% of the invoice value upfront, and the rest (minus a small fee) when the customer pays.

Unlike loans, factoring doesn’t create new debt—it simply accelerates access to cash that’s already owed to the business.

The Trade War Toll on Small Manufacturers—By the Numbers Trade wars hit manufacturers hard, especially the smaller players. Consider the impact:

According to the National Association of Manufacturers (NAM), tariffs in recent U.S.-China trade conflicts cost manufacturers over $57 billion between 2018 and 2021.

A 2023 survey by SCORE found that 58% of small manufacturers reported cash flow issues as their biggest challenge, exacerbated by rising input costs and delayed payments.

Tariffs on steel and aluminum alone have raised material costs by 10%–25%, depending on sourcing location and grade.

Payment terms have been lengthening, especially for B2B international orders, with many small manufacturers now facing average payment cycles of 45–60 days.

These disruptions don’t just create headaches—they create gaps in working capital that can slow or stop production entirely.

How Factoring Helps Small Manufacturers Bridge the Gap Fast Access to Cash Instead of waiting 60+ days for payment, manufacturers can get most of the invoice value within 24–48 hours. That can help cover materials, payroll, and urgent orders.

Avoiding New Debt Factoring doesn’t affect your debt-to-equity ratio or add to your liabilities—an advantage when applying for future financing or trying to stay lean during a volatile period.

Buffering Against Extended Payment Terms In sectors like electronics or industrial equipment, large buyers often demand longer terms. Factoring fills the working capital gap so you don’t have to delay supplier payments or production schedules.

Cash Flow to Offset Cost Increases If your materials cost has jumped by 15% due to tariffs, factoring helps ensure you can still purchase inventory without taking a hit to your credit line or delaying deliveries.

Freeing Up Time and Resources Many factoring companies also handle credit checks and collections. For small teams, this means more time focused on production and growth rather than chasing down late payments.

A Practical Example Let’s say a small plastics manufacturer supplies custom parts to a U.S.-based electronics company. They ship a $75,000 order with 60-day payment terms, but they need to purchase new resin (now 20% more expensive due to tariffs) and cover payroll next week.

By factoring the invoice, they receive $63,750 upfront (85% advance). That infusion keeps production moving, employees paid, and suppliers happy—without waiting two months for payment or resorting to high-interest credit.

Is Factoring Right for Your Manufacturing Business?

Factoring is especially effective for:

B2B manufacturers with reliable customer invoices over $10,000 per month

Companies with growing sales but cash flow bottlenecks

Manufacturers needing fast, recurring access to working capital

Those impacted by international trade tensions, delays, or tariffs

Final Thoughts Trade wars will continue to create unpredictability in global markets. But for small manufacturers, the ability to stay nimble and maintain strong cash flow is a game-changer. Accounts receivable factoring offers not just survival—but strategic advantage. Whether you’re sourcing new materials, expanding capacity, or just keeping your lines running, factoring can provide the capital you need to stay ahead—even when the global economy throws curveballs.

Versant has access to the capital necessary to fund larger factoring transactions than many other funding sources. Large deals!

Versant has access to the capital necessary to fund larger factoring transactions than many other funding sources.

Factoring Program Overview $100,000 – $30 Million Quick AR Advance No Audits No Financial Covenants No Long-Term Commitment Ideal for Companies with Strong Customers

We excel at LARGE & CHALLENGING deals : Turnarounds Historic Losses Customer Concentrations Poor Personal Credit Character Issues

Versant focuses on the quality of your client’s accounts receivable, ignoring their financial condition.

Analysis of James Clear’s “Atomic Habits” and Diverse Perspectives

This briefing document summarizes the main themes, important ideas, and critiques surrounding James Clear’s popular book, “Atomic Habits,” as gleaned from the provided sources.

1. Core Concepts of “Atomic Habits”:

“Atomic Habits” presents a practical framework for building good habits and breaking bad ones by focusing on small, incremental improvements (1% better each day) and the systems that drive those habits, rather than solely on goal setting. The book’s central structure revolves around the Four Laws of Behavior Change:

Make it Obvious (Cue): Design your environment to make good habit cues visible and bad habit cues invisible. Strategies include the Habits Scorecard, implementation intentions (“I will [BEHAVIOR] at [TIME] in [LOCATION]”), and habit stacking (“After [CURRENT HABIT], I will [NEW HABIT]”).

“Make the cues of good habits obvious and visible.” (Habits+Cheat+Sheet.pdf)

Make it Attractive (Craving): Increase the desire for good habits by pairing them with enjoyable activities (temptation bundling), joining supportive cultures, and creating motivation rituals. Conversely, reframe your mindset to find bad habits unattractive.

“Pair an action you want to do with an action you need to do.” (Habits+Cheat+Sheet.pdf)

Make it Easy (Response): Reduce friction associated with good habits by decreasing the number of steps, priming the environment, mastering decisive moments, using the Two-Minute Rule (downscaling habits), and automating where possible. Increase friction for bad habits.

“Decrease the number of steps between you and your good habits.” (Habits+Cheat+Sheet.pdf)

“Downscale your habits until they can be done in two minutes or less.” (Habits+Cheat+Sheet.pdf)

Make it Satisfying (Reward): Reinforce good habits with immediate rewards, use habit trackers (“don’t break the chain”), and ensure avoiding bad habits is enjoyable by seeing the benefits. For bad habits, make them unsatisfying, consider accountability partners, and habit contracts.

“Give yourself an immediate reward when you complete your habit.” (Habits+Cheat+Sheet.pdf)

“Keep track of your habit streak and “don’t break the chain.”” (Habits+Cheat+Sheet.pdf)

Clear emphasizes that lasting change comes from identity-based habits, where you first decide the type of person you want to be and then prove it to yourself with small wins. “Every action is a vote for the type of person you wish to become.” (Atomic Habits Summary)

2. Key Lessons and Principles:

The Power of Small Improvements: Clear argues that consistent 1% improvements daily lead to significant results over time (37 times better in a year). Conversely, small daily declines lead to near zero.

“if you can get 1 percent better each day for one year, you’ll end up thirty-seven times better by the time you’re done.” (Atomic Habits Summary)

“All big things come from small beginnings. The seed of every habit is a single, tiny decision.” (Atomic Habits Summary – quoting the book)

Focus on Systems, Not Just Goals: Goals are about desired outcomes, while systems are the processes that lead to those results. Clear contends that you fall to the level of your systems, so building effective processes is crucial for sustainable change.

“Goals are about the results you want to achieve. Systems are about the processes that lead to those results.” (Atomic Habits Summary)

“You do not rise to the level of your goals. You fall to the level of your systems.” (Atomic Habits Summary – quoting the book)

“The purpose of setting goals is to win the game. The purpose of building systems is to continue playing the game.” (Atomic Habits Summary – quoting the book)

Identity Shapes Habits: True behavior change comes from shifting your underlying beliefs and identity. Habits are reflections of your self-image.

“Your current behaviors are simply a reflection of your current identity.” (Atomic Habits Summary)

“To change your behavior for good, you need to start believing new things about yourself. You need to build identity-based habits.” (Atomic Habits Summary)

3. Critical Perspectives and Concerns:

One source, “My Problem with Atomic Habits by James Clear – The Wallflower Digest,” offers a strongly critical perspective on the book, raising several key concerns:

Lack of Authorial Credibility and Relatability: The reviewer questions James Clear’s self-proclaimed expertise, noting he “is not actually an expert qualified in anything” and seems to have always found habit-building easy. This lack of personal struggle makes his advice potentially less helpful for those who find it difficult.

“In the opener of the book he describes himself as a hyper organised, disciplined person who finds it easy to build good habits. This blew my mind because how would someone who’s brain just works like – who hasn’t had to try – be able to help someone like me, who has never been able to long-term stick to a routine of good habits?” (My Problem with Atomic Habits)

Repetitive and Superfluous Content: The reviewer argues the book’s core ideas could be conveyed in a much shorter format, describing it as “a mess of a book” and “insanely repetitive.” The constant directing to the author’s website is seen as off-putting.

“It reads like a blog post – or a newsletter – which is exactly what it started out as… the entire contents of it could be summed up in half a page.” (My Problem with Atomic Habits)

Oversimplification and Misapplication: The book is criticized for treating diverse behaviors (from binge eating to learning a language) as equal habits with the same simple solutions, failing to acknowledge the nuances of compulsive behaviors, psychological disorders, and lifestyle choices.

“Another problem with this book is that he conflates many things that are very different as equal habits with the same simple solutions.” (My Problem with Atomic Habits)

Lack of Rigorous Research: The reviewer points out the use of anecdotes, misrepresented examples, and citations from social media, questioning the book’s claim of being entirely research-led.

“The examples he uses to support his theories are often misrepresented to fit his narrative or based on nothing but anecdotes (and in one case an anecdote of an anecdote). He also cites Twitter and Reddit threads as sources!” (My Problem with Atomic Habits)

Insensitivity to Individual Differences: A significant criticism is the book’s apparent lack of awareness regarding factors like menstrual cycles and their impact on energy levels and consistency, potentially making the “don’t break the chain” mentality demotivating for some.

“If you have a menstrual cycle then your need for food, your focus, and your energy levels are going to fluctuate every few weeks. It’s not always going to be possible – or even healthy for you – to keep the same strict routine.” (My Problem with Atomic Habits)

Potentially Harmful Advice on Eating Disorders: The reviewer expresses concern that Clear’s advice on hyper-focusing on eating and feeling bad about binges could be triggering and irresponsible for individuals with eating disorders.

“James has some irresponsible advice on food and diet (losing weight, getting fit, building muscle) which definitely could be triggering for anyone with an eating disorder.” (My Problem with Atomic Habits)

Alignment with Unhelpful “All or Nothing” Mindset: The reviewer ultimately concludes the book reinforces a potentially damaging fitness and diet culture messaging that emphasizes “no pain no gain” and an “all or nothing” approach, which can be unproductive.

“I think the big reason this book has irritated me so much is that it buys into the most unhelpful of fitness and diet culture messaging – that no pain no gain, all or nothing kind of mindset.” (My Problem with Atomic Habits – Edit)

4. Positive Takeaways (Even from the Critique):

Despite the strong criticism, the reviewer in “My Problem with Atomic Habits” acknowledges some useful ideas:

Habit Stacking (Cueing Habits): The concept of linking new habits to existing ones to create a routine is seen as valuable.

“The main useful idea I got from this book was to cue habits, or what he called “Habit Stacking.” That is stringing together actions in your routine so that one good habit follows another.” (My Problem with Atomic Habits)

Making Habits Small and Easy: The emphasis on starting with very small, manageable steps is recognized as a helpful principle.

“My two takeaways from it were to make habits small and easy and to stack them to make a routine.” (My Problem with Atomic Habits)

5. Target Audience (According to the Critique):

The reviewer suggests the book may be most appealing to individuals who are already self-disciplined and find personal organization rewarding, but potentially less helpful for those who genuinely struggle with building habits.

Conclusion:

“Atomic Habits” offers a widely popular and seemingly accessible framework for habit formation based on four key laws. It emphasizes small, consistent improvements and the importance of systems and identity. However, critical perspectives highlight concerns about the author’s expertise, the book’s depth and research rigor, its oversimplification of complex behaviors, and its potential insensitivity to individual differences and specific challenges like hormonal fluctuations and eating disorders. While some core concepts like habit stacking and starting small are acknowledged as useful, readers should approach the book with a critical eye and consider their own unique circumstances and potential limitations of a one-size-fits-all approach to habit change.

According to the summary, what is the central idea of Atomic Habits in three sentences?

Explain the concept of “1 percent better every day” and why James Clear considers it significant.

What is the key difference that Clear draws between focusing on goals and focusing on systems?

Describe the two-step process Clear outlines for building identity-based habits.

List the four steps in the habit loop and briefly explain how they work together.

What are the “Four Laws of Behavior Change” for creating a good habit, as presented in the summary?

What are the inversions of the “Four Laws of Behavior Change” that can be used to break a bad habit?

According to the “My Problem with Atomic Habits” review, what are the main criticisms of the book? Provide at least two distinct points.

What is “habit stacking” as described in the excerpts, and how does it work?

According to the cheat sheet, what is the purpose of using a habit tracker, and what is the “never miss twice” rule?

Quiz Answer Key

Atomic Habits is a practical guide about making small, incremental improvements to your habits daily. It introduces the Four Laws of Behavior Change as a framework for building good habits and breaking bad ones. The book emphasizes that these tiny changes compound over time to produce significant results.

The concept of “1 percent better every day” means focusing on making small, daily improvements rather than seeking massive, overnight changes. Clear argues that while a 1 percent improvement might seem insignificant in the short term, these small gains accumulate exponentially over time, leading to remarkable progress after a year.

Clear states that goals are about the desired outcomes, while systems are the processes that lead to those outcomes. He argues that instead of solely focusing on achieving goals, individuals should prioritize building effective systems because you ultimately fall to the level of your systems, not the height of your goals.

The two steps for building identity-based habits are: first, decide the type of person you want to be; and second, prove it to yourself through small wins. By focusing on who you wish to become, your habits serve as votes for that identity, reinforcing your beliefs about yourself.

The four steps in the habit loop are cue, craving, response, and reward. The cue is the trigger that initiates the behavior, the craving is the motivational desire to change your state, the response is the actual habit you perform, and the reward is the satisfaction you gain from the response, which reinforces the connection between the cue and the behavior.

The Four Laws of Behavior Change for creating a good habit are: make it obvious (the cue), make it attractive (the craving), make it easy (the response), and make it satisfying (the reward). These laws provide a framework for designing habits that are more likely to be adopted and sustained.

The inversions of the Four Laws of Behavior Change for breaking a bad habit are: make it invisible (inversion of cue), make it unattractive (inversion of craving), make it difficult (inversion of response), and make it unsatisfying (inversion of reward). By making the cues of bad habits less noticeable and the behavior itself less appealing, easy, and rewarding, it becomes easier to break those habits.

One main criticism is that the book reads like a collection of blog posts or a newsletter and lacks the depth and research expected of a full book. Another criticism is that the advice is presented as universally applicable without acknowledging individual differences (like hormonal cycles or pre-existing conditions) and relies heavily on anecdotes rather than rigorous scientific evidence.

Habit stacking is a strategy where you link a new habit you want to form to a current habit you already have. The formula for habit stacking is: “After [CURRENT HABIT], I will [NEW HABIT].” This uses an existing routine as a cue for the new behavior, making it more likely to be remembered and performed.

According to the cheat sheet, the purpose of a habit tracker is to keep track of your habit streak and motivate you to maintain it by not “breaking the chain.” The “never miss twice” rule advises that if you fail to perform a habit on a given day, you should make sure to get back on track immediately the following day to avoid a longer lapse.

Essay Format Questions

James Clear argues that focusing on systems is more effective than focusing solely on goals. Analyze this argument, drawing upon concepts from the provided sources. Discuss the strengths and potential weaknesses of this approach in the context of personal development.

The Four Laws of Behavior Change (Make it Obvious, Attractive, Easy, Satisfying) and their inversions are central to Clear’s framework. Critically evaluate the practicality and effectiveness of these laws for habit formation and breaking, considering the insights and criticisms presented in the different sources.

The “My Problem with Atomic Habits” review raises several concerns about the book’s methodology and applicability. Analyze these criticisms in detail. To what extent do you find these critiques valid based on the other source materials and your own understanding of habit formation?

Explore the concept of “identity-based habits” as presented by James Clear. How does this approach differ from traditional goal-setting, and what are the potential benefits and challenges associated with building habits based on the type of person you want to become?

Synthesize the key strategies for building good habits and breaking bad habits presented across all the provided excerpts. Discuss which of these strategies appear most consistently emphasized and consider how they might be integrated into a comprehensive approach to personal change.

Glossary of Key Terms

Atomic Habit: A small, seemingly insignificant habit that is easy to do, but becomes a significant part of your system and contributes to substantial change over time due to compounding.

Compound Effect: The principle that small, consistent actions accumulated over time lead to remarkable results, either positive or negative.

Four Laws of Behavior Change: A framework presented by James Clear for building good habits, consisting of cue (make it obvious), craving (make it attractive), response (make it easy), and reward (make it satisfying).

Habit Loop: The neurological feedback loop that underlies every habit, consisting of a cue, a craving, a response, and a reward.

Habit Stacking: A strategy for building new habits by linking them to existing habits using the formula: “After [CURRENT HABIT], I will [NEW HABIT].”

Identity-Based Habits: Habits that are deeply connected to one’s desired identity and values. The focus is on becoming a certain type of person, and habits are the evidence of that identity.

Implementation Intentions: A planning strategy that involves specifying when, where, and how you will perform a particular behavior, often using the format: “I will [BEHAVIOR] at [TIME] in [LOCATION].”

System: The processes and routines that lead to results. Clear argues that focusing on building better systems is more effective for long-term improvement than focusing solely on goals.

Two-Minute Rule: A strategy for making habits easier to start by downscaling them until they can be completed in two minutes or less. The idea is to master the initiation of the habit.

Cue: The trigger or signal that initiates a habit. It can be time, location, a preceding event, or even another person.

Craving: The motivational force or desire that drives the habit. It’s the feeling you have to change your internal state.

Response: The actual action or habit you perform. This can be a thought, a feeling, or a physical behavior.

Reward: The satisfaction or benefit you gain from performing the habit. Rewards reinforce the habit loop, making the behavior more likely to be repeated in the future.

Reinforcement: Providing a reward or positive consequence immediately after a desired behavior to increase the likelihood of it being repeated.

Habit Tracker: A tool used to monitor whether a habit has been performed, often visualized as a calendar or list where you can mark your progress and “don’t break the chain.”

Friction: The difficulty or number of steps associated with performing a behavior. Increasing friction can help break bad habits, while reducing friction can help build good ones.

Temptation Bundling: A strategy to make habits more attractive by pairing an action you want to do with an action you need to do.

Motivation Ritual: Doing something you enjoy immediately before a difficult habit to make the difficult habit more appealing.

Commitment Device: A choice you make in the present that controls your actions in the future, often used to restrict options that could lead to bad habits.

Accountability Partner: A person who monitors your behavior and provides support and encouragement to help you stick to your habits.

Habit Contract: A formal agreement, often with an accountability partner, that outlines the costs of failing to adhere to your desired habits.

The Evolving Landscape of Small Businesses: 2025 Challenges & Opportunities

The small business sector in the United States stands at a critical juncture in 2025. While a sense of optimism prevails among many business leaders regarding the overall economic outlook, a closer examination reveals a complex environment characterized by persistent challenges alongside emerging opportunities. This report delves into the multifaceted impact of the current economic climate on these vital engines of the US economy, exploring the key headwinds they face, the avenues for growth they are pursuing, the crucial role of support systems, and the potential trends shaping their future. Inflation, supply chain vulnerabilities, labor shortages, and shifting consumer behaviors represent significant hurdles.

Conversely, the increasing adoption of technology, particularly in e-commerce and artificial intelligence, coupled with strategic partnerships and a renewed focus on customer experience, offers promising pathways forward. Furthermore, the support provided by government initiatives and the engagement of local communities are proving to be crucial factors in fostering the resilience of these enterprises. Looking ahead, the potential for economic shifts such as stagflation underscores the need for small businesses to remain agile and adaptable.

The Current Economic Climate and Small Business Sentiment:

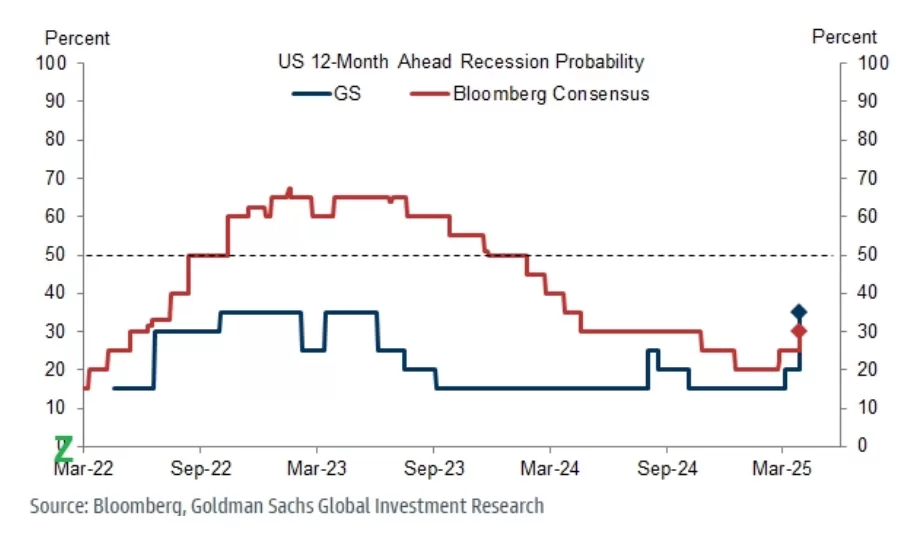

The economic landscape of the United States in 2024 and the anticipated trajectory for 2025 present a mixed picture for small businesses. Some analyses suggest that 2024 witnessed a moderation of inflation alongside continued growth in the Gross Domestic Product (GDP). This has contributed to an expectation of sustained economic expansion in 2025, provided that inflationary pressures remain under control. Indeed, business leaders appear to have shifted their focus from a cautious stance to one prioritizing growth, with a notable decline in concerns surrounding a potential recession. Surveys indicate that a significant majority of business leaders do not foresee a recession in 2025, a stark contrast to the sentiment expressed at the beginning of 2024. This improved outlook is partly attributed to the Federal Reserve’s interest rate cuts in late 2024 and signals of further easing, leading many to move past recessionary worries and concentrate on opportunities for expansion.

This optimistic sentiment is echoed by many small business owners, with a considerable percentage expressing confidence in their economic viability in 2025. However, this optimism exists in tandem with acknowledged challenges, such as the rising cost of doing business and evolving consumer trends. While national economic optimism has shown a strong rebound, the global economic outlook is perceived as more uncertain. Interestingly, the Small Business Index for the first quarter of 2025 experienced a slight dip, suggesting that despite the overarching optimism, some underlying concerns may be tempering overall confidence. Despite these individual business-level concerns, views regarding the health of the US and local economies have remained relatively stable. This could indicate that while small business owners might be facing specific operational challenges, they still perceive a degree of resilience and potential within their immediate economic environments.

Navigating the Headwinds: Key Challenges for Small Businesses:

3.1 Inflation and Rising Costs: A dominant concern casting a shadow over the small business landscape is the persistent issue of inflation and the escalating costs of operations. Reports indicate that inflation has reached record levels as a top concern for small businesses. The increasing costs associated with running a business are compelling many to raise their prices and implement measures to reduce operating expenses. A significant portion of small business owners anticipate that these costs are unlikely to decrease in 2025. The impact of inflation is also evident in consumer behavior, with some individuals choosing to curtail their spending at small businesses due to the higher cost of essential goods. Certain sectors are experiencing more pronounced price hikes than others, including finance, retail, construction, services, and professional services. The potential for new tariffs to be imposed further exacerbates these inflationary pressures, as tariffs typically lead to increased costs for imported goods, which are often passed on to consumers. Adding to the financial strain, the average monthly interest payments on credit cards for small businesses have also seen an increase. The convergence of record inflation concerns and the expectation of sustained high costs suggests that small businesses will continue to face significant pressure on their profitability, potentially necessitating difficult strategic choices regarding pricing, staffing levels, and future investments. The simultaneous rise in concerns about revenue alongside inflation indicates a challenging environment where businesses are not only grappling with higher expenses but are also finding it increasingly difficult to maintain their sales volumes, possibly pointing towards weakening consumer demand or heightened price sensitivity.

3.2 Supply Chain Disruptions: While the acute supply chain disruptions experienced in the immediate aftermath of the pandemic have somewhat subsided, critical issues continue to pose challenges for small businesses. Ongoing geopolitical instability and global trade uncertainties contribute to the volatility of supply chains. Disruptions stemming from wars, piracy, strikes, infrastructure failures, and adverse weather conditions continue to impede the smooth flow of goods. Ocean freight bottlenecks and congestion at global ports further compound these difficulties. The crisis in the Red Sea, for instance, has the potential to impact shipping costs and alter established trade routes. Moreover, the imposition of tariffs can directly disrupt supply chains and lead to inflated costs for businesses that rely on imported materials or components. In response to these persistent vulnerabilities, a growing number of businesses are adopting strategies such as reshoring and nearshoring to shorten their supply chains and reduce associated risks. Despite these efforts, managing inventory effectively remains a significant and ongoing challenge for many small businesses. The continued presence of global uncertainties implies that building resilient and agile supply chains is crucial for small businesses to effectively navigate unexpected disruptions. The increasing trend of reshoring and nearshoring signifies a strategic adaptation to these risks, potentially fostering growth in domestic manufacturing and supply sectors.

3.3 Labor Shortages and Workforce Management: Labor-related issues remain a dominant concern for business leaders across the United States. Small businesses are facing multifaceted workforce challenges, including difficulties in finding qualified candidates, retaining existing employees, and navigating the overall hiring process. Demographic shifts, particularly the retirement of the baby boomer generation, are contributing to significant talent gaps in various industries. Some experts suggest that immigration reform may be necessary to alleviate these workforce shortages and support business expansion. To attract and retain talent in this competitive environment, many small businesses are implementing strategies such as increasing wages, offering more flexible working arrangements, and enhancing employee benefits packages. The expectation is that labor markets will likely remain tight throughout 2025. In some instances, concerns about the quality of available labor have even surpassed inflation as the primary challenge for small business owners. The persistent difficulty in securing and retaining adequate staff is not merely a temporary setback but appears to be a more fundamental issue driven by demographic trends, necessitating long-term solutions focused on skills development and workforce expansion. Furthermore, the rising costs associated with labor are directly contributing to the increasing operational expenses for small businesses, thereby compounding the inflationary pressures they are already facing.

3.4 Shifting Consumer Behavior: The current economic climate is also influencing the behavior of consumers, presenting both challenges and opportunities for small businesses. The rising costs of essential goods and services are prompting many consumers to reduce their discretionary spending. This trend was particularly evident during the recent holiday season, where average consumer spending at small businesses saw a notable decrease. To navigate this evolving landscape, businesses are recognizing the need to adapt their marketing strategies to a more challenging online search environment. Consumers are also increasingly expecting seamless transitions between online and in-person shopping experiences. Moreover, there is a growing awareness among consumers regarding environmental issues, leading to a greater preference for businesses that prioritize sustainability and ethical practices. Finally, the trend towards consumers seeking more personalized products and services continues to gain momentum. The observed decline in consumer spending at small businesses, driven by the increasing cost of necessities, suggests a potential fundamental shift in consumer priorities. This necessitates that small businesses emphasize value, cultivate strong customer loyalty, and potentially broaden their offerings to include more essential goods or services. Conversely, the growing consumer emphasis on sustainability and ethical practices presents a distinct opportunity for small businesses to differentiate themselves from larger corporations by highlighting their local connections, ethical sourcing, and environmentally conscious operations.

4. Seizing Opportunities in a Changing Landscape:

4.1 E-commerce and Digital Presence: The realm of e-commerce continues to play an increasingly vital role in the retail sector, offering significant opportunities for small businesses. Given the growing proportion of retail sales occurring online, it is becoming essential for small businesses to establish and enhance their presence in the digital marketplace by offering their products and services through online channels. Effective online marketing strategies and active engagement on social media platforms are also crucial for reaching and connecting with potential customers. Notably, platforms such as TikTok and Instagram are increasingly being utilized not just for building brand awareness but also for direct client acquisition and facilitating sales conversions. The overall trend indicates that small businesses are intensifying their focus on digital marketing initiatives and expanding their e-commerce capabilities. To succeed in this digital-centric environment, it is paramount for small businesses to ensure they have a mobile-friendly and easily navigable website equipped with robust e-commerce functionalities that allow consumers to quickly find and purchase desired products or services from their mobile devices. The sustained and significant growth of e-commerce underscores the critical imperative for small businesses to invest strategically in their online presence. This investment is not solely for driving sales but also for enhancing brand visibility and fostering meaningful customer engagement, as consumers increasingly prioritize the convenience of online interactions. The emerging trend of leveraging social media platforms for direct sales signifies a blurring of the lines between traditional marketing and sales channels. This requires small businesses to develop integrated and agile strategies that effectively utilize social media not only for brand building but also for driving immediate transactional outcomes.

4.2 Technological Adoption and Innovation: The adoption of technology, particularly artificial intelligence (AI), is rapidly transforming the operational landscape for small businesses. AI is increasingly being implemented for a wide array of applications, including enhancing customer service, streamlining internal processes, and boosting overall productivity. AI-powered tools are proving valuable in tasks such as brainstorming new ideas, summarizing lengthy documents, automating meeting note-taking, and conducting advanced information searches. Many small businesses are also utilizing AI-driven chatbots and virtual assistants to improve the efficiency and responsiveness of their customer service operations. There is a prevailing sense of optimism among small business owners regarding the potential of AI to contribute to their future growth and success. However, the increasing reliance on technology also brings forth the critical importance of robust cybersecurity measures to protect sensitive data and mitigate the growing threat of cyberattacks. Beyond AI, other technological advancements, such as the rollout of 5G networks and the proliferation of remote collaboration tools, are also impacting small business operations. Furthermore, the adoption of various digital tools is playing a key role in enhancing operational efficiency and improving overall financial management for these enterprises. The accelerating adoption of AI by small businesses marks a significant evolution in their operational methodologies. This technological shift has the potential to democratize access to powerful tools, enabling even smaller enterprises to compete more effectively with larger counterparts in areas such as automation, data analysis, and customer engagement. The growing dependence on technology, especially AI and online operations, underscores the indispensable need for small businesses to prioritize investments in cybersecurity. Protecting their digital assets and maintaining customer trust is paramount for ensuring business continuity and long-term sustainability in an increasingly interconnected world.

4.3 Strategic Partnerships and Diversification: A significant proportion of businesses are actively exploring and planning to establish strategic partnerships and make targeted investments as a means of fostering growth and resilience. Diversifying the range of products and services offered is also recognized as a crucial strategy for catering to the evolving preferences and demands of consumers. The potential for mutually beneficial collaborations and mentorship opportunities between larger and smaller businesses is also gaining recognition. Expanding into new geographical markets within the domestic landscape represents another avenue for growth being considered by many businesses. Furthermore, some businesses are exploring mergers and acquisitions as a strategic pathway to achieve accelerated growth and market expansion. In the context of ongoing supply chain vulnerabilities, diversifying both sourcing and fulfillment networks is becoming increasingly important for building greater resilience and mitigating potential disruptions. The proactive pursuit of strategic partnerships and investments suggests a growing recognition among small businesses of the value of collaboration and external support in navigating the complexities of the current economic climate and achieving sustainable growth. The increasing emphasis on diversifying both product/service portfolios and sourcing strategies reflects a strategic imperative for small businesses to enhance their resilience by mitigating the inherent risks associated with fluctuating consumer demand and potential disruptions within their supply chains.

5. Small Business Resilience in Action: Case Studies:

A local restaurant, facing rising food costs due to inflation , has adapted by optimizing its menu to feature more seasonal and locally sourced ingredients, thereby reducing its reliance on volatile global supply chains and supporting local farmers. The restaurant has also invested in enhancing its online ordering system and partnered with local delivery services to cater to changing consumer preferences for convenience and at-home dining.

A small retail boutique, experiencing a slowdown in consumer spending on non-essential items , has successfully leveraged social media platforms to engage directly with its customer base, offering personalized styling advice and exclusive promotions to foster loyalty and maintain sales. The boutique has also emphasized its unique, small-batch offerings to differentiate itself from larger retailers.

A US-based manufacturing company, concerned about potential tariff increases and ongoing global supply chain disruptions , has made the strategic decision to reshore a portion of its production from overseas. This move not only mitigates the risks associated with international trade but also allows for greater control over quality and lead times.

A service-based business, operating in a sector facing significant labor shortages , has implemented AI-powered tools to automate routine administrative tasks and enhance communication with clients. This has allowed the existing staff to focus on higher-value activities and maintain service levels despite the challenges in recruitment.

A growing technology startup, facing the challenge of managing an expanding IT infrastructure within a tight budget, has opted for IT staff augmentation services. This approach provides the flexibility to access specialized technical expertise on an as-needed basis, proving more cost-effective than hiring full-time IT personnel.

A local non-profit organization dedicated to community outreach has adopted cloud-based software and online collaboration tools. This digital transformation has streamlined their internal operations, improved their ability to coordinate with volunteers, and enhanced their communication with the community they serve.

A small brewery, recognizing the increasing consumer interest in health and wellness , has expanded its product line to include a range of high-quality, non-alcoholic craft beverages. This diversification has allowed them to tap into a growing market segment and appeal to a broader customer base.

These examples, while representing a small fraction of the diverse adaptations occurring across the small business landscape, illustrate the proactive and innovative ways in which these enterprises are responding to the current economic pressures and capitalizing on emerging opportunities. The common thread running through these cases is a focus on agility, customer engagement, and the strategic adoption of technology and new business models.

6. Government and Community Support: Pillars of Small Business Stability:

6.1 Government Programs and Initiatives: The US Small Business Administration (SBA) plays a pivotal role in supporting the growth and resilience of small businesses through a variety of funding programs. These programs encompass loans designed for various purposes, including working capital, equipment purchases, and real estate; avenues for accessing investment capital; disaster assistance in the form of low-interest loans; surety bonds to facilitate contracting opportunities; and targeted grant programs. The SBA offers several distinct loan programs, such as the 7(a) loan, which is the most common type and can be used for a wide range of business needs; the 504 loan, providing long-term, fixed-rate financing for major assets; microloans for very small businesses and startups; disaster assistance loans for recovery from declared disasters; and loans specifically for military reservists called to active duty. Recognizing the financial challenges some small businesses face, the SBA also provides resources for those experiencing economic hardship, including access to free or low-cost financial counseling through its network of Resource Partners. While the Hardship Accommodation Plan (HAP) for COVID-19 Economic Injury Disaster Loans (EIDL) concluded in March 2025, other forms of assistance remain available. Additionally, the SBA and other organizations offer various grant programs tailored to specific industries or demographics, such as the Halstead Grant for silver jewelry artists, the Accion Opportunity Fund for underserved entrepreneurs, Amazon’s Black Business Accelerator Program, the Amber Grant Foundation for women entrepreneurs, and America’s Seed Fund for innovative technology startups. The broader governmental landscape, including potential tax and regulatory changes, can also significantly impact small businesses. Many small business owners have expressed a desire for simplification of the tax code and the extension of the 20% small business deduction. Key Table: Select SBA Funding Programs for Small Businesses

Program Name

Description

Use of Funds

Key Features

7(a) Loans

Most common SBA loan; flexible financing for various needs.

Working capital, equipment, real estate, debt refinancing.

Maximum loan amount typically $5 million; variety of terms and rates.

504 Loans

Long-term, fixed-rate financing for major fixed assets.

Purchase of equipment or real estate.

Typically involves a bank, a Certified Development Company (CDC), and the small business; favorable interest rates.

Microloans

Small loans for very small businesses and startups.

Working capital, inventory, supplies, furniture, fixtures, machinery, equipment.

Loans up to $50,000; administered through intermediary lenders.

Economic Injury Disaster Loans (EIDLs)

Low-interest loans to help businesses recover from declared disasters.

Working capital and normal operating expenses.

Available to small businesses in declared disaster areas; terms up to 30 years.

State Trade Expansion Program (STEP)

Grants to states to help small businesses increase their exports.

Export-related activities, such as trade show participation and marketing.

Administered by individual states; eligibility criteria vary.

Export to Sheets

6.2 Role of Local Communities and Consumer Support: The success and resilience of small businesses are inextricably linked to the support they receive from their local communities and individual consumers. Initiatives that encourage residents to shop locally and support community services play a vital role in keeping money circulating within the local economy. Studies have consistently shown that spending at local businesses generates a significantly greater economic impact within the community compared to spending at large chain stores. Supporting local businesses fosters entrepreneurship and strengthens the financial foundations of the community. Beyond the economic benefits, small businesses often contribute significantly to their communities by donating their time, financial resources, and in-kind contributions to various local groups, charities, schools, and other organizations. This involvement is not only important for the well-being of the community but also contributes to the personal satisfaction and fulfillment of small business owners. Consumers can actively support local businesses through various actions, such as shopping at local stores, dining at local restaurants, recommending local businesses to friends, writing positive online reviews, and participating in community events. By choosing to support local small businesses over large corporations, consumers directly invest in their own communities, fostering job creation, reinvestment, and a stronger local economy. The symbiotic relationship between small businesses and their local communities is a cornerstone of economic vitality and social well-being.

7. Potential Future Trends and Their Anticipated Impact:

7.1 Economic Trends: Looking ahead, the economic landscape for small businesses in 2025 is expected to be shaped by several key trends. While continued economic growth is anticipated by many, there is also the potential for inflation to accelerate, particularly given proposed policy changes such as tax cuts and tariffs. The trajectory of inflation will be closely watched, as a resurgence could necessitate further adjustments in business strategies. The impact of potential increases in tariffs remains a significant concern, especially for businesses that rely on international supply chains, as these could lead to higher costs for both businesses and consumers. Furthermore, the risk of stagflation, a scenario characterized by slow economic growth coupled with persistent high inflation, is being discussed by some economic analysts. Such an environment could present significant challenges for small businesses, impacting both their costs and consumer demand. The Federal Reserve’s monetary policy decisions, particularly regarding interest rates, will also play a crucial role in shaping the economic environment for small businesses, influencing borrowing costs and overall economic activity.

7.2 Technological Advancements and Digital Transformation: Technological advancements and the ongoing digital transformation will continue to profoundly impact small business operations and competitiveness. Artificial intelligence is expected to become even more integrated into various aspects of business, from customer service and marketing to operations and decision-making. The increasing accessibility and affordability of AI tools will likely drive further adoption across the small business sector. Automation of tasks, facilitated by AI and other digital tools, will be crucial for enhancing efficiency and reducing costs. As the reliance on technology grows, the importance of cybersecurity will only intensify, requiring businesses to invest in measures to protect their data and infrastructure. The trend of IT staff augmentation is also likely to continue, providing a flexible and cost-effective way for small businesses to manage their technology needs. Overall, the ability of small businesses to embrace and effectively utilize digital tools will be a key determinant of their success in the coming years.

7.3 Shifting Consumer Preferences: Evolving consumer preferences will continue to shape the small business landscape. The demand for personalized products and services is expected to grow, requiring businesses to leverage data and technology to tailor their offerings. Sustainability and ethical practices will likely become even more important to consumers, influencing their purchasing decisions and requiring businesses to adopt more environmentally and socially responsible approaches. The convenience and accessibility offered by online channels will continue to drive the growth of e-commerce, making a strong digital presence a necessity for most businesses. The rise of the gig economy may also present both opportunities and challenges for small businesses, affecting their workforce strategies and potentially creating new service models. Understanding and adapting to these evolving consumer preferences will be crucial for small businesses to maintain their competitiveness and relevance in the marketplace.

Conclusion:

The landscape for small businesses in the United States in 2025 is characterized by a complex interplay of challenges and opportunities. While the prevailing sentiment among many business leaders is optimistic, significant headwinds such as inflation, supply chain vulnerabilities, and labor shortages persist and demand careful navigation. The increasing adoption of technology, particularly in the realms of e-commerce and artificial intelligence, offers promising avenues for growth and efficiency. Strategic partnerships, diversification, and a keen focus on evolving consumer preferences will also be critical for sustained success. The support provided by government programs and the engagement of local communities remain vital pillars underpinning the stability and resilience of these enterprises. Looking ahead, potential economic shifts like accelerating inflation or even stagflation underscore the paramount importance of adaptability and strategic planning. Ultimately, the small business sector’s ability to embrace innovation, manage risks effectively, and respond agilely to the dynamic economic and technological environment will determine its continued vitality and its crucial contribution to the US economy.

Stagflation, a dreaded economic condition characterized by persistent high inflation combined with stagnant economic growth and high unemployment, poses a significant threat to businesses and the broader economy. While seemingly paradoxical, its recurrence in the 1970s serves as a stark reminder of its potential to wreak havoc. As global economic headwinds intensify, understanding the risks of stagflation is crucial for strategic decision-making.

Understanding Stagflation

Unlike typical economic downturns where inflation tends to subside, stagflation presents a unique challenge. The combination of rising prices and sluggish growth creates a complex environment where traditional policy tools become less effective.

Inflationary Pressures: Supply chain disruptions, geopolitical instability, and rising commodity prices can fuel persistent inflation. These factors can push input costs higher for businesses, forcing them to increase prices and further fueling the inflationary spiral.

Stagnant Growth: Weak consumer demand, reduced investment, and declining productivity contribute to sluggish economic growth. Businesses face difficulties in expanding operations, leading to potential layoffs and a rise in unemployment.

Policy Dilemma: Central banks are caught between a rock and a hard place. Raising interest rates to combat inflation can further stifle economic growth, while lowering rates to stimulate growth risks exacerbating inflationary pressures.

The Impact on Businesses:

Stagflation creates a challenging operating environment for businesses across various sectors.

Increased Costs: Rising input costs, including energy, raw materials, and labor, erode profit margins. Businesses may struggle to pass on these costs to consumers, leading to reduced profitability.

Reduced Demand: Consumer spending declines as inflation erodes purchasing power and economic uncertainty dampens confidence. Businesses may experience a drop in sales and revenue.

Investment Uncertainty: The unpredictable economic outlook deters investment in new projects and expansion. Businesses become more cautious, prioritizing short-term survival over long-term growth.

Labor Market Challenges: High unemployment and wage pressures can create difficulties in attracting and retaining skilled workers. Businesses may face increased labor costs and potential workforce shortages.

Supply Chain Vulnerabilities: Continued disruptions and volatility in global supply chains can lead to production delays and increased costs, further impacting business operations.

Mitigating the Risks:

While stagflation presents significant challenges, businesses can take proactive steps to mitigate its impact.

Cost Management: Implementing rigorous cost-control measures, optimizing supply chains, and improving operational efficiency can help businesses navigate rising input costs.

Pricing Strategies: Businesses must carefully balance price increases with maintaining competitiveness and consumer demand. Dynamic pricing strategies and value-added offerings can help mitigate the impact of inflation.

Diversification: Diversifying revenue streams, customer bases, and supply chains can reduce reliance on single markets or suppliers, minimizing vulnerability to economic shocks.

Financial Prudence: Maintaining strong cash reserves, managing debt levels, and focusing on financial stability are crucial during periods of economic uncertainty.

Strategic Planning: Scenario planning and stress testing can help businesses anticipate potential risks and develop contingency plans to navigate stagflationary conditions.

Technology Adoption: Investing in technology to improve efficiency, automate processes, and enhance productivity can help businesses reduce costs and improve competitiveness.

Looking Ahead:

The specter of stagflation looms as global economic uncertainties persist. Businesses must remain vigilant, adaptable, and proactive in navigating this challenging environment. By focusing on cost management, strategic planning, and operational resilience, businesses can better position themselves to weather the storm and emerge stronger.

The key is to remember that flexibility and rapid response to changing conditions are paramount. While predicting the future is impossible, preparing for a range of scenarios, including stagflation, is a critical component of responsible business leadership.