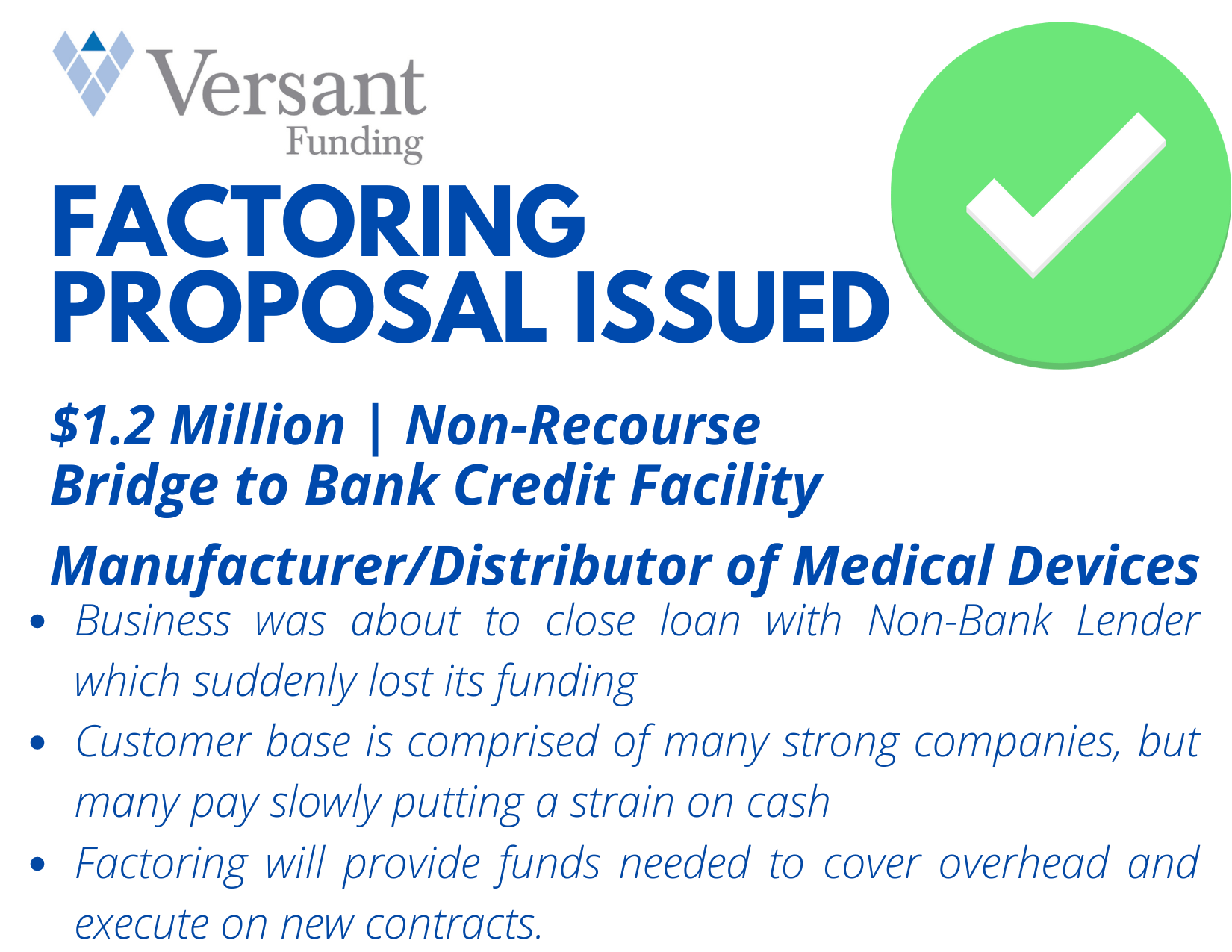

Our accounts receivable factoring program can help businesses meet payroll or other essential obligations in as quick as a week.

Funding Working Capital Shortfalls

Factoring Program Overview

$100,000 to $10 Million

Competitive Advance Rates

Non-Recourse

No Audits

No Financial Covenants

Most businesses with strong customers eligible

We specialize in difficult deals:

Start-ups

Weak Balance Sheets

Historic Losses

Customer Concentrations

Poor Personal Credit

Character Issues

We focus on the quality of your client’s accounts receivable, ignoring their financial condition. This enables us to move quickly and fund qualified businesses including Manufacturers, Distributors and a wide variety of Service Businesses in as few as 3-5 days. Contact me today to learn if your client is a fit.

The food production industry stands as a cornerstone of global commerce, providing sustenance to populations worldwide. Yet, despite its essential role, food producers are confronted with a myriad of financial challenges that threaten operational efficiency and long-term sustainability. As we delve into 2024, these challenges have been further exacerbated by a confluence of factors, ranging from supply chain disruptions to evolving consumer preferences. In this article, we explore the financing hurdles confronting food producers in the current landscape and identify strategies to surmount them. Financing Challenges of Food Producers.

Financing Challenges of Food Producers in 2024

Supply Chain Disruptions: A Persistent Challenge

One of the most pressing issues confronting food producers in 2024 is the enduring impact of supply chain disruptions. From raw material shortages to transportation bottlenecks, the intricacies of global supply chains have been stretched to their limits, resulting in increased costs and operational inefficiencies. For food producers, these disruptions translate into heightened financial strain as they grapple with rising procurement expenses and logistical complexities.

Escalating Input Costs and Inflationary Pressures

The relentless rise in input costs, including commodities, labor, and energy, has emerged as a significant financial headwind for food producers. Inflationary pressures, compounded by geopolitical tensions and economic uncertainties, have eroded profit margins and constrained cash flows. As food producers strive to maintain affordability amid escalating costs, securing adequate financing becomes imperative to sustain operations and remain competitive in the marketplace.

Regulatory Compliance and Sustainability Imperatives

In an era characterized by heightened regulatory scrutiny and sustainability imperatives, food producers face mounting pressures to adhere to stringent standards and invest in environmentally responsible practices. Compliance with food safety regulations, environmental mandates, and ethical sourcing requirements necessitates substantial investments in infrastructure, technology, and training. However, navigating the financial implications of regulatory compliance while maintaining profitability poses a formidable challenge for food producers.

Shifting Consumer Preferences and Market Dynamics

The evolving preferences of consumers, driven by factors such as health consciousness, ethical considerations, and convenience, present both opportunities and challenges for food producers. Adapting product portfolios, enhancing production processes, and embracing innovation are essential to remain relevant in a rapidly changing market landscape. However, the upfront investments required to pivot operations and meet evolving consumer demands can strain financial resources, particularly for small and medium-sized food producers.

Access to Capital and Financing Options

Amidst these multifaceted challenges, access to capital emerges as a critical determinant of success for food producers. Traditional lending institutions may exhibit reluctance to extend credit due to perceived risks associated with the industry’s inherent volatility and uncertainty. Moreover, stringent lending criteria and collateral requirements may pose barriers to entry for food producers, especially startups and enterprises with limited assets.

Strategies for Mitigating Financial Challenges

To navigate the financing challenges facing food producers in 2024, proactive measures and strategic initiatives are indispensable. Collaboration with financial institutions specializing in agribusiness lending can facilitate access to tailored financing solutions tailored to the unique needs of food producers. Additionally, leveraging government-sponsored programs, such as agricultural subsidies and grants, can provide supplemental funding to support capital investments and operational enhancements. Financing challenges.

Furthermore, embracing technological innovations, such as blockchain-enabled supply chain management and precision agriculture technologies, can optimize efficiency, reduce costs, and enhance competitiveness. Engaging in strategic partnerships and vertical integration initiatives can also unlock synergies and diversify revenue streams, thereby mitigating financial vulnerabilities and fostering resilience in an uncertain environment.

Conclusion

As food producers confront an array of financing challenges in 2024, proactive adaptation and strategic foresight are essential to overcome obstacles and thrive in a dynamic marketplace. By embracing innovation, fostering collaboration, and exploring diverse financing options, food producers can navigate the complexities of the current landscape and position themselves for long-term success. Amidst the turbulence of the times, resilience, agility, and innovation will be the hallmarks of food producers poised to seize opportunities and surmount challenges in the pursuit of sustainable growth and prosperity.

Video: What is the structure of a factoring facility?

Terms vary by factor.

Most usually consist of an initial advance of 75% to 90% against accounts receivable.

Factoring fees (aka discount rates) range from 1% to 3% of the invoice for each month the invoice is outstanding (this may be broken down into five, 10 or 15-day increments).

Lower rates are typically reserved for recourse factors with a greater focus on business performance. Some factors charge both a factoring fee as well as an interest rate on funds advanced. Be careful to read the fine print as some factors may include other charges.

Most factoring facility terms range from zero to 24 months and range in size from $10,000 to more than $10 million per month in factoring volume. Different factors are focused on the low and high end of this range. Many factors require a client to commit to factor a certain volume each month. Some factors set no cap on their facility and will allow fundings to grow as the client’s business grows if they keep selling to creditworthy companies.

First lien on accounts receivable will be required (at a minimum), so ask your client early in the process if they have any outstanding liens on their AR. It may be possible to have an incumbent lender subordinate its lien on AR to allow factoring, but success rates are usually low. Most factoring facility terms range from zero to 24 months and range in size from $10,000 to more than $10 million per month in factoring volume.

Different factors are focused on the low and high end of this range. Many factors require a client to commit to factor a certain volume each month. Some factors set no cap on their facility and will allow fundings to grow as the client’s business grows if they keep selling to creditworthy companies.

First lien on accounts receivable will be required (at a minimum), so ask your client early in the process if they have any outstanding liens on their AR. It may be possible to have an incumbent lender subordinate its lien on AR to allow factoring, but success rates are usually low. The Approval Process For a non-recourse factor, little information over and above a recent accounts receivable aging and customer list may be necessary to obtain a proposal. The factor will use this information to assess the quality of the customer base.

Recourse factors, which perform more of a hybrid analysis, will likely require a standard commercial financing package, including current and historic financials, so they can underwrite the business performance as well as the accounts receivable. Term sheets issued in hours to a few days are common.

The Funding Process Your client will continue to do business as they always have: shipping products, completing services and invoicing their customers. From there, the invoices will be sent to the factor. For a notification factor, the invoice will include payment instructions to the factoring company. The factor will verify the invoice by contacting the customer.

Upon verification, the factor will advance your client 75% to 90% of the invoice — often the same day the invoice is issued. When the factor receives payment from the customer, your client will be sent the “rebate” (the remaining 10% to 25%, less the factoring fee). Most factors will fund their clients as often as daily, or less frequently as needed by the client. Initial funding under a factoring facility is often in less than a week. Once a facility is in place, funding usually takes place the same day a new invoice is issued.

Advantage – Speed Most factors put no restrictions on how funds may be used, but a few uses can include:

• Project financing • Business growth financing • Business acquisition financing • Bridge financing • Financing working capital needs • Realization of supplier discounts • Preparation for high season • Crisis management • Debtor-in-possession (DIP) financing Approvals in hours/days not weeks Flexible use of proceeds Non-recourse – It reduces the credit risk of the seller.

The working capital cycle runs smoothly as the factor immediately provides funds on the invoice. Non- recourse – can reduce collection staff/AR tracking Improves liquidity and cash flow in the organization. It leads to improvement of cash in hand.

This helps the business to pay its creditors in a timely manner which helps in negotiating better discount terms. It reduces the need for the introduction of new capital in the business. Elastic credit facility

Many factors will not put a firm cap on facility size, but will allow the facility to grow as AR base grows Can be helpful with rapidly growing businesses

Disadvantages: Cost – Factoring fees (aka discount rates) range from 1% to 3% of the invoice for each month the invoice is outstanding Inability to leverage other assets An ABL facility may allow advances against Inventory, Equipment and CRE A true factor will only advance against AR Providing factor access to customer base

Factoring: The solution to your client’s working capital problem $100,000 – $10 Million Non-Recourse – No Personal Guaranty Most Businesses with Strong Customers are Candidates Start-Ups, Rapidly Growing, Highly Leveraged, Customer Concentrations, Weak Personal Credit/ Character Issues are all Eligible Small Business Lending Account Receivable Factoring Asset Based Lending

Video – Factoring: The Solution to your Working Capital Problems

Chris Lehnes 203-664-1535 clehnes@chrislehnes.com

Chris Lehnes 203-664-1535 clehnes@chrislehnes.com